- Tool and Technology: How Samera Does It

- 5 Ways Accounting Technology Accelerates Growth

- Evolution of Accounting Technology: A Brief Overview

- Importance of Accounting Tech Integration

- Offshoring and AI: Future Proof your Accountancy Firm

- The Current State of Accounting Technology

- Assessing Your Firm’s Technological Needs

- Selecting the Right Accounting Tools

- Guide to Successfully Implementing Accounting Technology

- Leveraging Technology for Client Services

- Navigating the Tech Evolution in Accounting

- Safeguarding Financial Integrity with Cybersecurity and Data Protection

- Measuring the ROI of Technology Investments

- Conclusion– Mastering Technology for Accounting Firms

- Download the Workbook

- How to Fill in the Tool and Technology Workbook

- Bibliography

Key Takeaways

- Automate Repetitive Work: Use the right technology to handle bookkeeping, invoicing, and reporting automatically.

- Strengthen Client Communication: Set up real-time portals and CRM systems to keep clients in the loop.

- Analyse the Data: Use reporting tools to spot trends and make smarter, real-time decisions.

- Switch to Cloud-Based Tools: Move your systems online for remote access and easier scaling.

- Upgrade Your Tech Stack: Regularly review and adopt new tools to stay ahead of the curve.

Welcome to Module Four of our ‘Grow Your Accountancy Firm’ course, where we delve into the space of Accounting Technology and Tools for Efficiency. In today’s fast-paced business landscape, leveraging cutting-edge technology isn’t just an option – it’s a necessity for growth and business continuity.

With our earlier modules comprehensively covering the accounting industry overview, the key pillars of successful business strategy, i.e., organizational vision and mission, and the pieces you need to put in place to build a strong accounting team, you are all set to take the next step in building an Unstoppable accounting firm. With accounting tech decisions sorted, your team will be well equipped to make greater stride, boost productive, and enhance efficiency, all while enabling growth and profitability for your accounting firm.

Tool and Technology: How Samera Does It

Let’s look at how we do it. In this episode of the Unstoppable podcast, Arun and Chris look at how technology has changed the way we work over the last 20+ years. From what is most important to us to look for in technology to where we think the industry is going, this is how we do it.

The Going Global Podcast

July 2024

5 Ways Accounting Technology Accelerates Growth

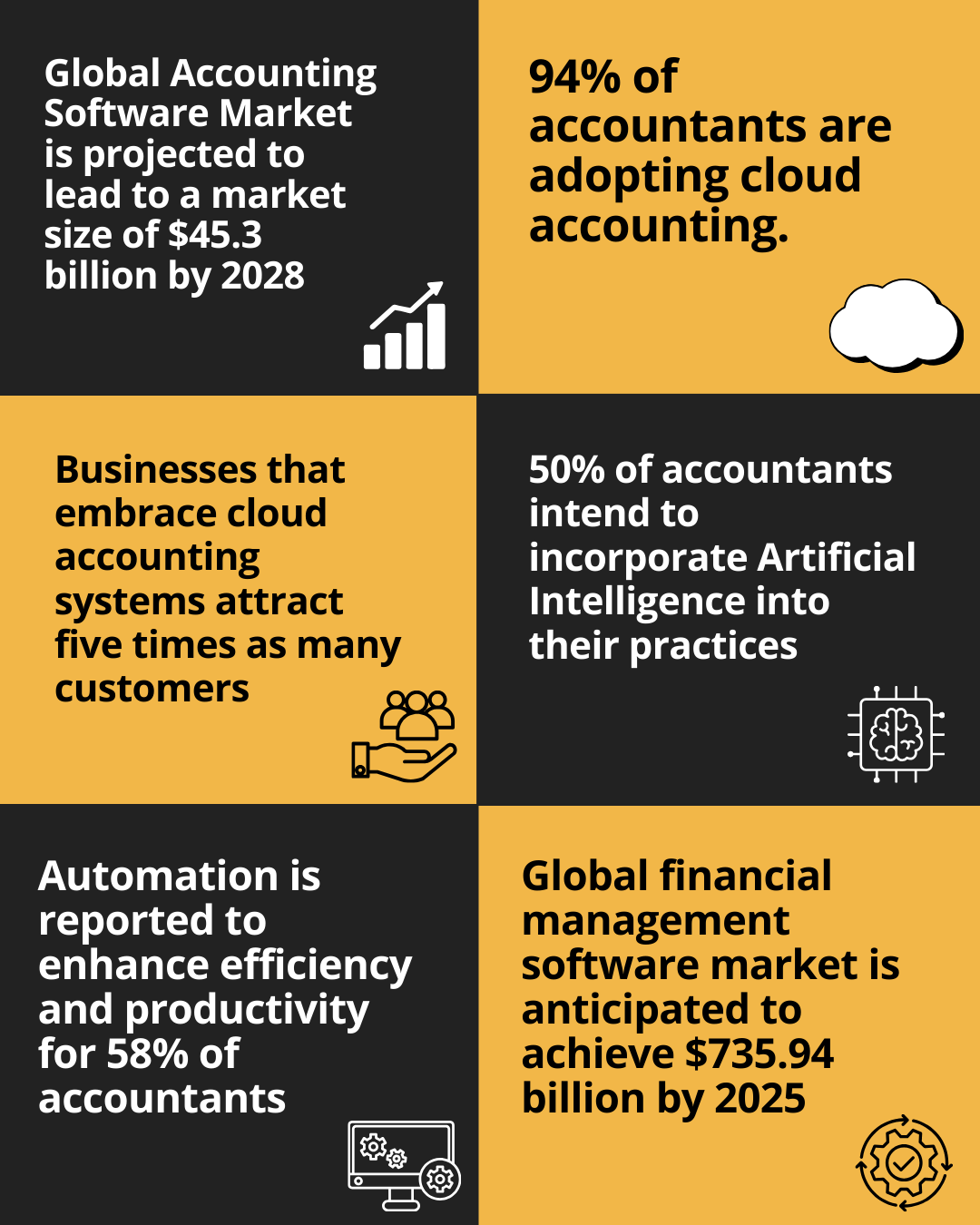

The anticipated growth of the Global Accounting Software Market is projected to lead to a market size of $45.3 billion by 2028, with a Compound Annual Growth Rate (CAGR) of 19.6% throughout the forecast period [1]. For accounting firms, embracing cutting-edge technology is a strategic move that propels firms forward. The symbiotic relationship between technology and growth is evident in the following ways:

- Enhanced Productivity: Automation of routine tasks allows accountants to focus on strategic analysis and value-added services, amplifying productivity and enabling the handling of a larger client portfolio.

- Client Relationship Management: Technology facilitates more meaningful client interactions. With real-time updates and collaborative platforms, accountants can provide timely insights, fostering stronger client relationships and client retention.

- Data-Driven Decision Making: Advanced analytics tools empower accountants with deep insights into financial data, enabling informed decision-making. This analytical prowess contributes to proactive financial management and strategic planning.

- Global Reach: Cloud-based accounting transcends geographical limitations, enabling firms to service clients globally. This expanded reach opens up new markets and clientele, a vital driver for the growth of any accountancy firm.

- Operational Efficiency: Integrating technology streamlines internal processes, reducing the margin for error and enhancing operational efficiency. This not only results in time and cost savings but also positions the firm as a reliable and efficient partner in the eyes of clients.

Evolution of Accounting Technology: A Brief Overview

The landscape of accounting technology has undergone remarkable transformations over the years, shaping the way firms operate and thrive. Let’s trace this evolution through four key milestones:

- Manual Ledger Systems (Pre-20th Century): In the pre-digital era, accounting relied heavily on manual ledger systems, where every entry was meticulously recorded by hand.

- Introduction of Spreadsheets (1980s): The 1980s witnessed a game-changer with the advent of spreadsheets, notably Excel, streamlining calculations and data organization.

- Integration of Accounting Software (1990s-2000s): The 1990s and 2000s marked the shift towards specialized accounting software, simplifying complex financial processes and increasing accuracy.

- Cloud-Based Accounting (2010s-Present): The current era is dominated by cloud-based solutions, fostering collaboration, accessibility, and real-time data management. In fact, the adoption of cloud accounting stands at an impressive 94% among accountants, showcasing its convenience and accessibility [2].

Click here to read our article on The Impact and Challenges of AI on Accounting Outsourcing.

Importance of Accounting Tech Integration

In this context, the integration of advanced tools and technology emerges as the linchpin for efficiency and competitiveness. Facts show, businesses that embrace cloud accounting systems attract five times as many customers compared to those depending on traditional methods [3].

Over the course of this module, we will explore the transformative impact of technology on workflows, collaboration, security, scalability, and the overall competitive edge of your accountancy firm.

- Streamlined Workflows: Modern accounting tools automate repetitive tasks, reducing manual errors, and enhancing overall workflow efficiency.

- Real-Time Collaboration: Cloud-based platforms facilitate real-time collaboration among team members and clients, fostering seamless communication and decision-making.

- Data Security: Integrating secure accounting technology ensures the confidentiality and integrity of sensitive financial data, building trust with clients.

- Scalability: As your firm grows, scalable technology allows for easy expansion without compromising on efficiency, adapting to the evolving needs of your clientele.

- Competitive Edge: Staying abreast of the latest accounting technology gives your firm a competitive edge, attracting clients who seek forward-thinking and technologically adept financial partners.

In this module, we’ll explore these aspects and equip you with the knowledge and skills needed to harness the full potential of accounting technology for the sustained growth of your accountancy firm.

Offshoring and AI: Future Proof your Accountancy Firm

The Current State of Accounting Technology

In the ever-evolving landscape of accounting, the tech stack adopted by accounting teams serves as the bedrock for sustained growth and long-term success. Here, we try to understand the current state of accounting technology, dissecting the pivotal elements that shape the future of accountancy firms.

Accounting technology has transcended beyond mere digitization; it has become the cornerstone for achieving efficiency, accuracy, and client satisfaction. The current tech stack embraced by accounting teams is not just a toolset; it’s a strategic asset that empowers firms to navigate the complexities of modern finance. As we delve into the nuances of the latest trends and advancements, it becomes evident that these technologies are not just about staying current; they are a blueprint for future success.

5 Key Tech Trends Shaping up Accounting Technology

In this section, we delve into the pulse of the latest trends steering the evolution of accounting technology. These aren’t just abstract notions; they are pragmatic shifts shaping the daily operations of accountancy firms. From the seamless collaboration afforded by cloud computing to the analytical prowess of artificial intelligence, each trend is a building block in the tech foundation transforming traditional practices.

As we unpack each trend, you’ll gain a clear understanding of how these advancements are not just tools but strategic navigators, propelling accountancy into a realm of enhanced efficiency and responsiveness. Here are 5 latest accounting tech trends:

Cloud Computing: The adoption of cloud computing has revolutionized how accounting data is stored, accessed, and processed. It provides the flexibility of real-time collaboration, ensuring that accountants and clients can seamlessly work together regardless of geographical constraints. This trend not only enhances accessibility but also lays the foundation for secure and scalable data management.

Artificial Intelligence (AI): AI has woven its way into the fabric of accounting, automating repetitive tasks and unlocking the power of data analysis. From predictive analytics to anomaly detection, AI empowers accountants to move beyond routine functions, focusing on strategic insights and decision-making. A case in point: Within the next few years, 50% of accountants intend to incorporate Artificial Intelligence into their practices, underscoring the expanding potential of this technology [4]. The integration of AI algorithms enhances accuracy, reduces errors, and amplifies the overall efficiency of financial processes.

Automation: Automation, a stalwart in the modern accounting arsenal, streamlines mundane tasks such as data entry, invoice processing, and reconciliation. In fact, automation is reported to enhance efficiency and productivity for 58% of accountants, liberating their time for more advanced tasks [5]. By automating these routine functions, accounting teams can redirect their efforts towards value-added activities, fostering productivity and client satisfaction. Automation not only accelerates processes but also minimizes the risk of human error.

Blockchain Technology: Blockchain emerges as a transformative force, particularly in enhancing the security and transparency of financial transactions. Its decentralized ledger system ensures the integrity of financial data, reducing the risk of fraud and unauthorized access. As blockchain gains prominence, it heralds a new era of trust and accountability in accounting practices.

Data Analytics and Business Intelligence: The integration of robust data analytics and business intelligence tools equips accountants with deeper insights into financial data. By leveraging these tools, accountancy firms can extract actionable intelligence, facilitating data-driven decision-making. This trend not only augments the advisory role of accountants but also positions them as strategic partners in the business planning process.

Click here to read our article The Ultimate Tech Stack for UK Accounting Firms.

Transformation of Traditional Accounting Practices

Moving forward, we transition into a realm where technology ceases to be a mere support function and becomes a catalyst for the metamorphosis of traditional accounting practices. From accelerated speed and precision to reimagined client collaboration, we unravel the tangible transformations at play.

Here are 5 ways accounting technology is reshaping how accountancy firms operate, adapt, and thrive in an ever-changing space.

Accelerated Speed and Efficiency: The adoption of cloud computing and automation accelerates the speed at which accounting tasks are executed. Real-time data access and automated workflows reduce turnaround times, enabling accounting teams to respond swiftly to client needs and market dynamics.

Enhanced Accuracy and Compliance: AI and automation contribute significantly to the accuracy of financial data. By automating compliance checks and leveraging AI-driven validation, accountants can ensure adherence to regulations and standards, mitigating the risk of errors and non-compliance.

Improved Client Collaboration: Cloud-based platforms facilitate seamless collaboration between accountants and clients. Clients can access financial data in real-time, contribute to the process, and engage in meaningful discussions. This enhances client satisfaction, loyalty, and the overall client-accountant relationship.

Strategic Decision-Making: The infusion of AI and data analytics transforms accountants into strategic advisors. The ability to derive actionable insights from vast datasets empowers accountants to contribute meaningfully to business strategy and financial planning, transcending the traditional role of number-crunching.

Adaptability to Industry Changes: The agility afforded by advanced accounting technology enables firms to adapt swiftly to industry changes. Whether it’s regulatory shifts, technological advancements, or market fluctuations, the tech-enabled accounting team is better positioned to navigate uncertainties and proactively address challenges.

Assessing Your Firm’s Technological Needs

According to Sage’s Practice of Now report, a majority of accountants, about 56%, acknowledge that technology is playing a pivotal role in boosting their productivity [6]. In this chapter, we explore the crucial task of assessing your firm’s technological needs. This isn’t about chasing trends; it’s a pragmatic approach to calibrating the tech stack that will empower your team to navigate the complexities of modern finance.

The right technology is not a one-size-fits-all equation; it’s a tailored ensemble that aligns with the unique needs and goals of your firm. In this exploration, we will guide you through the process of evaluating your current technological infrastructure and identifying potential gaps. This evaluation is not just a technological decision, it’s a strategic move that can make the difference between stagnation and growth, between mediocrity and excellence in the competitive landscape of modern accountancy.

As we delve into the intricacies, keep in mind that the right technology is not just a support system; it’s the cornerstone for building a resilient and thriving accountancy firm.

Click here to read our article on 5 Ways in which Robotic Process Automation (RPA) is Reshaping the Accounting Workforce.

Evaluating Your Current Technological Infrastructure

The first step towards equipping your team for success is a critical examination of your existing technological foundation. From the capability of your current software to the agility of your systems, each determinant is a crucial puzzle piece in the larger tech landscape. This isn’t just about what you have; it’s about understanding how well it aligns with your operational goals.

We explore five key determinants that should guide your evaluation, providing a solid foundation for informed decision-making in the realm of accounting technology.

- Software Capability and Integration: Consider the software that powers your firm’s operations. Are these tools seamlessly integrated, or do they operate in silos? Without fluid integration, your team expends unnecessary effort in manual data transfers, diminishing overall efficiency. An integrated system ensures a smooth flow of data, reducing errors and promoting collaboration across your firm.

- Data Security Measures: Moving forward, examine your data security measures. In the intricate realm of accounting, safeguarding sensitive financial information is paramount. A breach could jeopardize legal compliance and tarnish your firm’s reputation. Thus, evaluating the robustness of your security measures becomes a cornerstone in fortifying your technological foundation.

- Scalability of Systems: Scalability is another critical aspect. Is your current tech infrastructure equipped to handle the growth trajectory of your firm? Scalable systems are not just accommodating; they are a strategic asset. They allow your firm to expand seamlessly without compromising on operational efficiency. Ensuring that your tech can adapt to the evolving demands of your business is crucial for sustained growth.

- User Training and Adoption: User training and adoption play a pivotal role in maximizing the benefits of your tech stack. Even the most sophisticated tools are only effective when your team utilizes them optimally. Investing in comprehensive user training ensures proficiency, empowering your team to harness the full potential of available technologies.

- Compliance with Regulatory Standards: Finally, regulatory compliance cannot be overlooked. Is your tech stack aligned with the latest industry regulations? Staying current with compliance standards is not just a legal requirement; it’s a safeguard against potential liabilities. Ensuring that your technology complies with industry standards fortifies the legal soundness of your firm.

Identifying Technology Gaps for Successful Integration

As we transition to the second section, we dive into the crucial task of identifying technology gaps that may be impeding the optimal functioning of your accounting firm. These aren’t theoretical gaps; they are real-world challenges that can stifle efficiency and hinder growth. From data security concerns to integration issues, each area explored is a potential turning point in your firm’s technological journey.

This section delves into 5 areas where these gaps often emerge, emphasizing their impact within the accounting function:

- Integration Challenges: Transitioning to the identification of technology gaps, our first concern lies in integration challenges. Are your various software applications struggling to collaborate seamlessly? Integration challenges lead to data silos, hindering real-time information flow. Addressing these challenges ensures a more cohesive and collaborative environment within your firm.

- Outdated Software and Legacy Systems: Outdated software and reliance on legacy systems pose significant obstacles. Continuing dependence on such systems not only compromises efficiency but exposes your firm to security vulnerabilities. The solution lies in transitioning to modern solutions that align with contemporary technological standards, fortifying your tech infrastructure against potential risks.

- Inadequate Data Analytics Capabilities: Data analytics capabilities form the backbone of informed decision-making in accounting. If your current tools fall short in delivering actionable insights, your firm might be missing critical opportunities. Upgrading or diversifying data analytics capabilities enables your team to extract meaningful intelligence from financial data.

- Limited Mobility and Remote Access: The demand for mobility and remote access has become increasingly prevalent. If your current systems hinder remote work, productivity suffers. Enhancing mobility ensures your team can work seamlessly from any location, promoting flexibility and collaboration.

- Lack of Automation in Repetitive Tasks: Finally, manual task domination in repetitive activities indicates a need for automation. Automating routine tasks not only reduces errors but allows your team to redirect their efforts towards strategic initiatives, amplifying productivity and efficiency.

Through a meticulous examination of these determinants and gaps, you pave the way for an informed decision-making process that aligns your technological foundation with the growth trajectory of your accounting firm.

Selecting the Right Accounting Tools

In the last two chapters, we’ve tried to offer enough context into why the ideal tech stack can make all the difference for your firm. This chapter navigates the key area of tool selection, emphasizing the need for a thoughtful and tailored approach in equipping your accounting team.

The immense impact of technology on the sector is evident as the global accounting software market is anticipated to achieve an impressive $735.94 billion by 2025 [7].

Choosing the right accounting tools is akin to building the foundation of a sturdy structure. It’s about aligning technology with the unique needs and goals of your accounting firm. The selection directly impacts your team’s efficiency, adaptability, and overall productivity. In this chapter, we delve into the critical aspects of choosing the most suitable accounting software and tools, unraveling the criteria and an overview of popular choices in the market.

5 Criteria for Choosing Accounting Software and Tools

The selection process begins with defining criteria that resonate with the specific needs of your accounting firm. Each criterion addresses a distinct challenge, offering a problem-solution relationship tailored to the nuances of the accounting business.

- Scalability: As accounting firms grow, existing tools might struggle to keep pace, hindering expansion. The solution lies in opting for tools that scale with your business, ensuring seamless growth without compromising efficiency. Scalability guarantees your technology aligns with the evolving needs of your firm.

- User-Friendliness: Complex interfaces and intricate features can lead to a steep learning curve for your team. The remedy lies in prioritizing user-friendly tools that enhance accessibility and ease of use. A simple interface ensures quicker adoption and utilization, maximizing the benefits of the chosen tools.

- Integration Capabilities: Incompatibility between different software applications can result in data silos and hinder collaboration. The solution involves choosing tools with robust integration capabilities. Seamless data flow between applications fosters a cohesive working environment, eliminating silos and promoting collaboration.

- Data Security Measures: Inadequate security measures expose your firm to the risk of data breaches. The answer is to prioritize tools with robust data security features. A secure platform safeguards sensitive financial information, ensuring compliance with regulatory standards and preserving the integrity of your data.

- Customization Options: Generic tools may not cater to the specific needs and workflows of your accounting firm. The solution involves opting for tools with customization options. Tailoring the software to align with your unique processes enhances efficiency and ensures a seamless integration into your firm’s operations.

Overview of 5 Popular Accounting Tools

In this section, we provide an overview of five major accounting tools that have proven instrumental in making accounting teams more productive and efficient. Each tool is a testament to the transformative power of technology in streamlining the accounting function.

- QuickBooks: QuickBooks simplifies accounting tasks, offering features for invoicing, expense tracking, and financial reporting. It is user-friendly and widely used by small to medium-sized businesses. Demonstrating its user-friendliness and popularity, QuickBooks maintains its dominance in the accounting software claiming over three-fourth of the total market share [8].

- Xero: Xero is known for its cloud-based accounting features, providing real-time collaboration, automatic bank reconciliations, and a user-friendly interface.

- FreshBooks: FreshBooks is renowned for its invoicing capabilities, time tracking, and expense management. It streamlines financial tasks for freelancers and small businesses.

- Wave: Wave offers free accounting software with features like invoicing, expense tracking, and receipt scanning. It is ideal for small businesses and startups.

- Sage Intacct: Sage Intacct is a robust cloud-based accounting solution suitable for midsize and enterprise-level businesses. It offers advanced features for financial management, reporting, and automation.

By exploring these criteria and popular tools, you gain a comprehensive understanding of the considerations that should guide your tool selection process, empowering your accounting team for enhanced efficiency and long-term success.

Guide to Successfully Implementing Accounting Technology

When it comes to the accountancy function, implementing the right technology is a strategic leap toward enduring growth. This chapter serves as a practical guide, unraveling the complexities of technology implementation in accounting firms. Successful adoption is not just about incorporating new tools; it’s a transformative process that reshapes how teams operate and positions firms for long-term success.

According to LXA’s Martech Report, the primary obstacle hindering investment in technology is insufficient integration, ranking as the number one barrier [9]. The implementation of technology is a strategic necessity for accounting firms aspiring to achieve sustained growth. Beyond mere process optimization, the right technology enhances adaptability and client service.

In this chapter, we explore the critical steps in the implementation process, uncovering best practices and insights into overcoming common challenges specific to the accounting business.

5 Best Practices for Seamless Accounting Tech Implementation

Implementing new technology in an accounting firm demands a thoughtful approach. Here are 5 best practices crucial for successful accounting technology integration.

- Comprehensive Staff Training is paramount in the accounting function. Effective use of new technology hinges on the team’s understanding of its intricacies. Prioritizing comprehensive staff training programs equips the team with the necessary skills, ensuring a smooth transition and minimizing disruptions in workflow.

- Phased Rollouts offer a solution to abrupt changes that can disrupt ongoing operations. Introducing new technology gradually allows the team to acclimate, providing room to address challenges before full-scale implementation.

- Clear Communication Channels are essential to prevent miscommunication leading to confusion, resistance, and potential errors in the implementation process. Establishing clear communication channels ensures that the team is well-informed about changes, benefits, and ongoing support structures, fostering a collaborative approach.

- Customization to Fit Workflow addresses the challenge posed by generic solutions that may not seamlessly align with the unique workflow of an accounting firm. Customizing the technology to fit specific processes ensures that the tools enhance, rather than disrupt, the established workflow.

- Continuous Monitoring and Feedback are vital post-implementation. Ongoing evaluation is necessary to address emerging issues and optimize usage. Implementing continuous monitoring and feedback mechanisms allows for regular assessments, user feedback, and proactive resolution of challenges.

5 Common Challenges During Implementation and How to Overcome Them

Despite careful planning, challenges may arise during technology implementation. Understanding these challenges and having strategies to overcome them is crucial.

- Resistance to Change is a common challenge as team members may resist adopting new technology. Addressing resistance through comprehensive training, clear communication of benefits, and emphasizing the positive impact on efficiency and client service can help overcome this challenge.

- Integration Issues may arise during the integration of new technology with existing systems, leading to data discrepancies and disruptions. Prioritizing compatibility and conducting thorough testing before implementation ensures a seamless integration to prevent data silos and inconsistencies.

- Data Security Concerns may arise during the transition to new technology. Selecting technology with robust security features and transparently communicating the measures in place to protect data helps alleviate concerns.

- Downtime and Productivity Loss can occur during implementation, impacting client service and overall productivity. Planning implementations during periods of lower activity and employing phased rollouts can minimize downtime and facilitate a smoother transition.

- Budget Overruns pose a risk with unforeseen expenses during implementation potentially straining the budget. Conducting thorough cost assessments before implementation, establishing a contingency budget, and ensuring financial plans are resilient to unexpected expenses can mitigate this challenge.

By incorporating these best practices and understanding potential challenges, accounting firms can navigate the implementation of technology with resilience, ensuring a smooth transition towards a more efficient and technologically empowered future.

Leveraging Technology for Client Services

Did you know that an overwhelming 83% of accountants express the sentiment that clients have become more demanding in recent times [10]. For accountancy firms, technology can prove to be a powerful means to foster stronger client relationships, inspire trust, and streamline client acquisition and retention. This chapter unravels the ways in which accounting firms can leverage technology to enhance client services, creating a more meaningful and dynamic client experience that goes beyond the numbers.

Accounting firms stand to gain not just operational efficiency but also enhanced client trust and satisfaction by strategically incorporating technology into their client service framework. In this chapter, we explore how technology becomes the catalyst for stronger client relationships, making client acquisition and retention more seamless and impactful.

5 Ways Accounting Technology Enhances Client Services

The infusion of technology transforms the landscape of client services in accounting, offering a more personalized, efficient, and communicative experience.

- Personalized Reporting is a critical enhancement that ensures reports resonate with individual client needs. By utilizing technology that allows for tailored reporting, firms can provide more relevant and insightful financial information, deepening client satisfaction.

- Real-Time Data Access addresses the challenge of delays in accessing crucial financial data. Implementing technology that provides real-time data access empowers clients to make informed decisions promptly, enhancing their confidence in the accuracy and timeliness of accounting services.

- Improved Communication Channels through modern tools like secure client portals, instant messaging, or video conferencing enhance communication efficiency. This fosters a more transparent and collaborative client-firm relationship, improving overall client satisfaction.

- Workflow Automation for Efficiency is a strategic enhancement that tackles delays and errors associated with manual processes. Automation streamlines repetitive tasks, ensuring accuracy and efficiency, allowing the team to focus on strategic aspects of client management.

- Client Education Platforms offer clients a deeper understanding of their financial landscape. Through webinars, tutorials, or interactive content, these platforms empower clients with knowledge, fostering a more informed and engaged client base.

5 Accounting Tech Services Adding Value to Clients

In this section, we delve into real-world examples of technology-driven services that go beyond conventional offerings, adding significant value to clients and setting accounting firms apart in terms of client servicing.

- Automated Bookkeeping Services: Automated bookkeeping services go beyond the conventional by leveraging advanced accounting software. This not only ensures accuracy in financial record-keeping but also frees up valuable client time for strategic business focus. The automation of routine bookkeeping tasks enables clients to redirect their efforts towards more critical aspects of their business, enhancing overall efficiency and productivity.

- Predictive Analytics for Financial Planning: The integration of predictive analytics tools offers clients forward-looking financial insights. This goes beyond traditional financial planning by enabling clients to anticipate challenges and opportunities in their financial landscape. By harnessing the power of data-driven predictions, clients can make informed decisions, optimize resources, and proactively plan for the future, elevating the strategic financial planning aspect of client services.

- Mobile Accounting Apps for On-the-Go Access: The provision of mobile accounting apps is a tangible way to add value to clients. In a fast-paced business environment, on-the-go access to key financial data is invaluable. Mobile accounting apps empower clients with real-time information wherever they are, facilitating quick decision-making and enhancing overall client satisfaction through convenience and accessibility.

- Cybersecurity Consultation Services: In the digital age, cybersecurity is paramount. Offering cybersecurity consultation services adds substantial value by ensuring the protection of client financial data. This service goes beyond traditional accounting roles, providing clients with insights into safeguarding sensitive information. By addressing cybersecurity concerns, accounting firms become trusted partners in protecting clients from potential cyber threats, thereby enhancing overall client trust and confidence.

- Virtual CFO Services: Virtual CFO services utilize technology to provide clients with strategic financial guidance, budgeting, and forecasting. This goes beyond the standard accounting scope by offering clients access to high-level financial expertise without the cost of a full-time CFO. This service empowers clients with insights and recommendations that are typically reserved for larger enterprises, fostering a sense of partnership and adding significant value to their financial decision-making processes.

By understanding how technology can enhance client services and exploring concrete examples of value-driven tech services, accounting firms can not only meet but exceed client expectations, building lasting relationships and a strong reputation in the competitive landscape of financial services.

Navigating the Tech Evolution in Accounting

Staying abreast of technological changes in accounting is key for accounting firms and teams. This chapter delves into the reasons why accounting firms must prioritize keeping their teams updated on evolving accounting tech. Additionally, we explore the pivotal role a robust tech infrastructure plays in driving long-term growth for accounting firms.

Highlighting the imperative for adaptation, 57% of accountants identify technology literacy as the most crucial skill for future professionals [11]. In a digital era, technological changes in accounting are rapid and transformative. To ensure sustained growth, accounting firms must not only embrace these changes but also equip their teams with the knowledge and skills to navigate the evolving landscape.

This chapter unfolds strategies for staying updated with technological advancements and emphasizes the indispensable nature of continuous learning in the ever-changing world of accounting technology.

Strategies for Staying Updated with Technological Advancements

Technological advancements in the accounting field are continuous and rapid. Staying updated is not just a best practice; it’s a survival strategy. Here are five strategies to help accounting firms keep pace with ongoing technological changes.

- Continuous Training Programs: Embrace a culture of continuous learning within the firm. Implement regular training programs to keep the team updated on the latest accounting software, tools, and industry trends. This proactive approach ensures that team members are well-equipped to handle new technologies as they emerge, fostering adaptability.

- Industry Networking and Conferences: Encourage participation in industry conferences and networking events. These platforms offer insights into emerging technologies, industry best practices, and the experiences of other professionals. Networking provides a valuable opportunity for sharing knowledge, staying informed, and building a network of industry contacts.

- Utilization of Online Resources: Leverage online resources such as webinars, forums, and industry blogs. The internet is a treasure trove of information on the latest technological developments. Encouraging the team to explore and engage with these resources ensures a constant influx of knowledge, enhancing the firm’s ability to adapt to new technologies.

- Collaboration with Tech Providers: Foster strong relationships with technology providers. Establishing direct lines of communication with software developers and vendors ensures that the firm is among the first to receive updates and insights into upcoming features or changes in accounting technology. This collaboration facilitates a proactive approach to tech integration.

- Cross-Functional Training: Promote cross-functional training. Encourage team members from different functional areas within the firm to share their insights and experiences with technology. This interdisciplinary approach fosters a holistic understanding of technological advancements, ensuring that the entire firm is well-versed in the evolving tech landscape.

The Importance of Continuous Learning and Adaptation

Continuous learning and adaptation are not just desirable traits; they are indispensable in the context of the accounting business. Here are five points highlighting the significance of continuous learning in the ever-evolving world of accounting technology.

- Adaptability to Regulatory Changes: Regulatory frameworks in accounting often evolve alongside technological advancements. Continuous learning ensures that the team remains adaptable to changes in compliance requirements, reducing the risk of non-compliance and ensuring the firm operates within the bounds of the law.

- Enhanced Client Service Delivery: Technological changes directly impact how services are delivered to clients. Continuous learning enables the team to stay ahead of client expectations by incorporating the latest tools and methodologies. This not only enhances client satisfaction but also positions the firm as a tech-savvy and forward-thinking service provider.

- Efficiency and Productivity Gains: Regular training and adaptation to new technologies result in increased efficiency and productivity. Team members who are well-versed in the latest tools can navigate tasks more efficiently, reducing the time and effort required for various processes. This not only optimizes internal operations but also contributes to the firm’s overall profitability.

- Competitive Edge in the Industry: Continuous learning gives accounting firms a competitive edge in the industry. Firms that adapt swiftly to technological changes position themselves as leaders and innovators. This not only attracts clients seeking cutting-edge services but also distinguishes the firm in a competitive market.

- Future-Proofing the Firm: The accounting landscape will continue to evolve. Continuous learning is the key to future-proofing the firm. By fostering a culture of adaptability and staying ahead of technological changes, accounting firms ensure their relevance and sustainability in the long run.

By implementing effective strategies for staying updated and recognizing the importance of continuous learning, accounting firms can not only survive but thrive in an era of rapid technological evolution.

Safeguarding Financial Integrity with Cybersecurity and Data Protection

In the digital age, where technology forms the backbone of accounting operations, the paramount importance of cybersecurity and data protection cannot be overstated. This chapter underscores the critical role these measures play in fortifying the integrity of sensitive financial data. It emphasizes how a robust cybersecurity protocol is not just a legal obligation but a fiduciary responsibility, instilling client confidence and paving the way for long-term growth.

As accounting firms increasingly rely on technology for operational efficiency, the focus on cybersecurity and data protection becomes non-negotiable. In fact, accounting firms face a significantly higher risk, being three times more likely to be targeted by cyberattacks compared to the average business [12].

The vulnerability of sensitive financial data necessitates a vigilant approach to safeguarding it. Beyond mitigating risks, a robust cybersecurity protocol becomes a cornerstone for client confidence and, consequently, the sustained growth of accounting firms.

Click here to read our article on 6 Cybersecurity Challenges for Accountants and How to Tackle Them.

Critical Role of Cybersecurity Measures

The accounting industry bears a substantial burden, with the average cost of a data breach reaching a staggering $2.3 million [13]. Protecting sensitive financial data is paramount in the digital landscape, and several measures play a pivotal role in achieving this:

Encryption Protocols: Implementing robust encryption protocols is akin to placing financial data in a digital vault. Encryption transforms data into unreadable code, ensuring that even if unauthorized access occurs, the data remains indecipherable. This cryptographic safeguard provides a robust layer of defense against potential breaches.

Multi-Factor Authentication: Enhancing access security is crucial in preventing unauthorized access to sensitive data. Multi-factor authentication adds an additional layer of defense by requiring multiple forms of verification before granting access. This significantly reduces the risk of unauthorized access, especially in an era where cyber threats are becoming more sophisticated.

Regular Security Audits: Continuous vigilance is key to cybersecurity. Regular security audits act as health check-ups for an accounting firm’s digital infrastructure. Conducting periodic assessments helps identify vulnerabilities and ensures that cybersecurity measures evolve in tandem with emerging threats. It is a proactive approach to maintaining a resilient security posture.

Employee Training Programs: Mitigating human errors, often the weakest link in cybersecurity, requires comprehensive employee training programs. These initiatives sensitize staff to potential threats, instill security-conscious habits, and empower them to recognize and report potential security breaches. Employees become a proactive line of defense against cyber threats through education and awareness.

Incident Response Planning: Preparedness for contingencies is a critical component of cybersecurity. No system is infallible, and having a well-defined incident response plan ensures that the firm can respond swiftly and effectively in the event of a cybersecurity incident. This minimizes potential damages and facilitates a coordinated and efficient response.

Best Practices for Data Protection and Compliance

Maintaining compliance with data privacy regulations and upholding data protection standards is not just a legal obligation but a testament to an accounting firm’s commitment to ethical practices:

Regular Data Backups: Mitigating data loss is fundamental to data protection. Regularly backing up sensitive financial data ensures that, in the event of a cybersecurity incident, data can be restored, minimizing the impact of potential loss. This practice provides a safety net against unexpected data disruptions.

Data Access Controls: Ensuring restricted access is crucial for protecting sensitive financial data. Implementing stringent access controls ensures that not all personnel require access to all data. By limiting access based on roles and responsibilities, firms reduce the risk of unauthorized data exposure and ensure data confidentiality.

Compliance with Privacy Laws: Legal adherence to data privacy regulations is mandatory. Staying informed about and complying with regulations such as GDPR, HIPAA, or other regional laws ensures that the firm operates within legal frameworks. Adherence to privacy laws safeguards the firm against legal repercussions and reinforces ethical business practices.

Secure Vendor Relationships: Mitigating third-party risks is crucial in the digital ecosystem. Many accounting firms collaborate with external vendors. Ensuring that these vendors follow robust cybersecurity measures is essential. Secure vendor relationships contribute significantly to overall data protection efforts and prevent vulnerabilities introduced by external partners.

Data Encryption During Transmission: Securing data in transit adds an extra layer of protection. Beyond encrypting data at rest, ensuring that data is encrypted during transmission mitigates the risk of interception. This is particularly crucial when exchanging sensitive financial information over networks, enhancing the overall security posture of data.

Cybersecurity and data protection are foundational elements for the trust that underpins client relationships and the long-term growth of accounting firms. Implementing these measures and best practices fortifies digital fortresses, ensuring data integrity in an era where it is non-negotiable.

Measuring the ROI of Technology Investments

Demonstrating substantial cost benefits, accounting automation solutions generally yield a return on investment within a relatively short span of 6-18 months [14].

However, these investments should not be arbitrary; they need to be measured and assessed for their financial impact. Understanding how to assess the financial impact of these investments is critical for making informed decisions that contribute to long-term growth.

Beyond the allure of innovation, understanding the return on investment is vital for sound financial decision-making. This chapter explores the significance of evaluating the ROI of technology investments and how it serves as a compass for sustainable growth in the dynamic realm of accounting.

5 Methods to Evaluate ROI for Technology Implementations

Determining the return on investment requires specific methodologies tailored to the unique needs of accounting firms. Here are five methods that accounting owners can employ to make sense of their technology investments, offering meaningful insights into the financial impact of their technology investments:

- Cost-Benefit Analysis (CBA): In the domain of accounting, where precision and efficiency are paramount, conducting a thorough Cost-Benefit Analysis (CBA) is indispensable. This method involves meticulously quantifying the costs associated with implementing a new technology, such as software licenses or training expenses, against the expected benefits. For accounting firms, these benefits may include time saved in data processing, improved accuracy in financial reporting, and enhanced client services. CBA offers a comprehensive financial snapshot, aiding owners in making informed decisions based on tangible outcomes directly relevant to the accounting business.

- Return on Investment (ROI) Formula: The classic ROI formula finds profound relevance in accounting, where quantifiable results are essential. By applying the ROI formula owners can gauge the profitability of their technology investments in clear, percentage terms. This method is particularly effective for accounting firms looking to assess the direct financial impact of their technology implementations, providing a straightforward measure of the efficiency of the expenditure in relation to net profit.

- Payback Period Calculation: For accounting firms keen on understanding when their technology investments will start yielding positive financial returns, the Payback Period Calculation becomes a valuable tool. This method offers a tangible timeframe within which the initial investment is expected to be recouped through generated returns. A shorter payback period is especially advantageous for accounting firms, ensuring a quicker realization of financial benefits and a faster transition to a positive ROI.

- Net Present Value (NPV): Accounting for the time value of money is crucial in financial decision-making for accounting firms. Net Present Value (NPV) offers a nuanced approach by discounting future cash flows to their present value. This method helps owners assess the true financial viability of technology implementations over time, considering factors like inflation and interest rates. In the context of accounting, where precise financial planning is imperative, NPV provides a nuanced perspective on the long-term financial impact of technology investments.

- Benchmarking Against Industry Standards: Accounting firms operate in a competitive landscape where efficiency and accuracy are differentiators. Benchmarking technology investments against industry standards allows owners to contextualize their financial impact. This method provides insights into how the firm’s technology implementations compare to industry peers in terms of efficiency gains, cost-effectiveness, and overall financial impact. For accounting businesses, this comparative analysis serves as a strategic tool for staying competitive and ensuring that technology investments align with or exceed industry benchmarks.

In employing these methods tailored to the nuances of the accounting business, owners can navigate the complexities of technology investments with precision, aligning their financial decisions with the specific goals and demands of the industry.

4 Strategies to Achieve Cost Efficiency with Accounting Tech

While evaluating the ROI is crucial, achieving optimal cost efficiency is equally important. Striking a balance between costs and benefits ensures that technology investments contribute to long-term growth without becoming financial burdens.

Here are four strategies to help accounting firms navigate this delicate balance:

- Prioritize Scalability: Prioritizing scalable solutions ensures that technology investments grow alongside the firm’s needs. Scalable systems can accommodate increased workloads without significant additional costs, providing a cost-efficient approach to long-term expansion.

- Invest in Training Programs: Enhancing the skills of the workforce through training programs is an investment that pays dividends. Well-trained personnel maximize the efficiency gains from technology implementations, reducing the risk of underutilized or misused tools. This strategic investment in human capital ensures the technology’s long-term benefits are fully realized.

- Regular Technology Audits: Conducting regular audits of existing technology infrastructure helps identify redundancies, inefficiencies, or outdated systems that may be inflating costs. An optimized and up-to-date tech stack ensures that resources are directed where they yield the most significant returns, contributing to long-term cost-effectiveness.

- Embrace Cloud Solutions: Cloud-based solutions offer scalability and flexibility while minimizing upfront infrastructure costs. By shifting to cloud technologies, accounting firms can achieve cost efficiency, benefit from automatic updates, and adapt seamlessly to changing business requirements. This approach aligns with a dynamic and cost-effective tech strategy.

We learnt that measuring the ROI of technology investments is a strategic imperative for accounting firms. Employing tailored methods for assessment and balancing costs with efficiency gains positions firms for sustainable growth in an ever-changing technological landscape.

Conclusion– Mastering Technology for Accounting Firms

As we conclude this module, it’s essential to reflect on the transformative journey through the integration of technology in accounting practices. We’ve explored how technology acts as a catalyst, driving growth, efficiency, and competitiveness for accounting firms.

This chapter encapsulates the cause-and-effect relationship between embracing modern technology and charting a path toward sustained success in the dynamic landscape of accounting.

Reiterating 7 Key Reasons to Integrate Modern Accounting Technology

For accountancy firms, the integration of modern technology stands as a linchpin for growth and resilience. Let’s recap seven key takeaways that underscore the profound significance of incorporating cutting-edge technology into accounting practices:

- Efficiency Amplification: Modern tools amplify efficiency, reducing manual efforts and streamlining workflows. The automation of repetitive tasks allows accountants to focus on strategic endeavors, fostering productivity and accuracy.

- Enhanced Data Security: Technological advancements ensure robust cybersecurity measures, safeguarding sensitive financial data. The integration of encryption, multi-factor authentication, and secure cloud solutions fortifies the digital perimeters of accounting firms.

- Strategic Decision-Making: Advanced analytics and reporting tools empower accountants with actionable insights. Real-time data access facilitates strategic decision-making, enabling firms to respond swiftly to market changes and emerging opportunities.

- Client-Centric Services: Technology facilitates personalized reporting, improved communication channels, and seamless collaboration. These client-centric services not only enhance satisfaction but also contribute to client acquisition and retention.

- Cost-Efficiency and Scalability: Scalable solutions and cloud technologies align with the financial objectives of accounting firms. They offer cost-efficiency by minimizing upfront infrastructure costs and adapting seamlessly to changing business requirements.

- Competitive Edge: Embracing technological advancements positions accounting firms at the forefront of the industry. A tech-savvy approach not only attracts clients seeking innovative services but also distinguishes firms in a competitive market.

- Future-Proofing the Firm: Continuous learning and adaptation to technological changes are crucial for future-proofing accounting firms. Staying ahead in the technological curve ensures relevance and sustainability in the long run.

5 Motivators to Embrace Accounting Technological Advancements

To stay competitive and efficient, accounting firms must not only acknowledge technological advancements but actively embrace them. Here are five motivations driving firms to earnestly pursue accounting technology:

- Adaptability to Evolving Regulations: The dynamic regulatory landscape requires accounting firms to adopt technology that facilitates compliance. Integrated systems help navigate changing regulations and ensure adherence to legal frameworks.

- Client Expectations and Preferences: Clients increasingly expect seamless, technology-driven services. Embracing technology aligns accounting firms with client preferences, contributing to client satisfaction, retention, and positive word-of-mouth referrals.

- Globalization and Remote Work Trends: The rise of remote work and globalization necessitates technology that supports collaboration across distances. Cloud-based solutions and virtual communication tools enable firms to operate efficiently in a distributed work environment.

- Efficiency Gains in Complex Operations: As accounting operations become more intricate, manual processes prove inadequate. Technology offers advanced functionalities, such as AI-powered data analysis and automation, optimizing efficiency in handling complex financial tasks.

- Strategic Positioning in the Industry: Firms that proactively adopt technology position themselves as industry leaders. This strategic positioning not only attracts clients but also establishes a reputation for innovation and forward-thinking practices.

Download the Workbook

Download our Technology Implementation Workbook below to kickstart the process of upgrading your accounting firm’s technology.

By using the information provided in this module and conducting your own research, you’ll gain insights into the latest technological trends in the accounting industry. You’ll also develop your own strategies to address these trends effectively and position your firm for success. Additionally, you’ll analyze competitors to identify best practices and areas for improvement.

Ultimately, you’ll create a comprehensive plan outlining the technology tools, software, and infrastructure needed to support your firm’s growth objectives. This workbook will help you implement the strategies outlined in this course with clarity and purpose.

Download the Workbook:

How to Fill in the Tool and Technology Workbook

How do I get started with using the Technology Implementation Workbook?

Starting with the Technology Implementation Workbook involves a structured approach to planning, executing, and managing the integration of new technology within your organization or team. This workbook can serve as a guide to ensure that the technological change is aligned with your business objectives, efficiently implemented, and effectively adopted by all stakeholders. Here’s how to get started:

- Define Your Objectives

- Identify Needs: Clearly articulate the reasons for implementing new technology. This could be to improve efficiency, enhance service quality, meet regulatory requirements, or stay competitive.

- Set Goals: Define specific, measurable goals that you aim to achieve with the technology implementation. These should align with your broader business objectives.

- Assess Current State

- Technology Audit: Conduct an audit of your current technology landscape, including hardware, software, and systems in use. Identify gaps, redundancies, and areas for improvement.

- Skill Assessment: Evaluate the current technology skills and capabilities of your team. This will help in identifying training needs and potential resistance to change.

- Research and Selection

- Market Research: Investigate available technology solutions that meet your identified needs. Consider factors such as cost, scalability, compatibility with existing systems, and vendor support.

- Stakeholder Input: Involve key stakeholders in the selection process, including IT staff, end-users, and management. Their input can provide valuable insights and foster buy-in.

- Implementation Planning

- Project Plan: Develop a detailed project plan for the technology implementation, including timelines, milestones, responsibilities, and resources required.

- Risk Management: Identify potential risks and challenges associated with the implementation and plan mitigation strategies.

- Training and Support

- Training Program: Design a training program to upskill your team on the new technology. This should be tailored to different user levels and learning styles.

- Support Structure: Establish a support structure to assist team members during and after the implementation. This could include a help desk, FAQ resources, and regular check-ins.

- Change Management

- Communication Plan: Create a communication plan that keeps all stakeholders informed about the progress of the implementation, changes to workflows, and how the technology will benefit them.

- Feedback Mechanism: Implement a mechanism for collecting feedback from users on the technology’s usability, problems encountered, and suggestions for improvement.

- Testing and Rollout

- Pilot Testing: Conduct pilot testing of the new technology with a small group of users to identify any issues before a full rollout.

- Phased Rollout: Consider a phased rollout of the technology, starting with one department or team before extending it across the organization.

- Evaluation and Iteration

- Performance Metrics: Define metrics to evaluate the success of the technology implementation against your initial objectives.

- Continuous Improvement: Use feedback and performance data to make iterative improvements to both the technology and how it’s used within your organization.

- Document and Share Learning

- Documentation: Document the process, challenges encountered, solutions implemented, and lessons learned during the technology implementation.

- Knowledge Sharing: Share these insights within your organization to inform future technology projects and initiatives.

Starting with the Technology Implementation Workbook is about taking a methodical approach to ensure that new technology is thoughtfully integrated into your organization’s workflow, addressing both technical and human factors to achieve successful outcomes.

What information should I gather before completing the workbook?

Before completing the Technology Implementation Workbook, gathering comprehensive information is crucial for informed decision-making and strategic planning. Here’s a checklist of the key information you should collect:

- Business Objectives and Requirements

- Strategic Goals: Understand the strategic goals of your organization and how the technology implementation aligns with these goals.

- Specific Needs: Identify the specific business needs and challenges the technology aims to address. This could include efficiency improvements, cost reductions, enhanced security, or better customer service.

- Current Technology Landscape

- Existing Systems: Catalog existing hardware, software, and platforms currently in use. Note any limitations, issues, or gaps in these systems.

- Integration Requirements: Determine how the new technology will need to integrate with current systems. This includes data migration needs and compatibility considerations.

- User Needs and Stakeholder Expectations

- User Profiles: Identify the primary users of the new technology, including their roles, technology proficiency, and daily tasks.

- Stakeholder Input: Gather input from all stakeholders, including management, IT staff, end-users, and clients (if applicable), on their expectations and requirements from the technology implementation.

- Technical Requirements and Specifications

- Functionality Needs: Detail the specific functionalities the new technology must provide to meet your business objectives.

- Performance Criteria: Define the performance criteria, such as speed, reliability, and user-friendliness, that the technology must meet.

- Budget and Resources

- Budget Constraints: Determine the budget available for the technology implementation, including both initial costs and ongoing expenses.

- Resource Availability: Assess the internal and external resources available for the project, including personnel, time, and technology infrastructure.

- Compliance and Security Requirements

- Regulatory Compliance: Identify any regulatory compliance requirements that the technology implementation must adhere to, such as data protection laws.

- Security Needs: Outline the security features and protocols needed to protect your organization’s data and operations.

- Training and Support Needs

- Training Requirements: Assess the training needs for users of the new technology, considering different skill levels and learning preferences.

- Support Infrastructure: Determine the type of support infrastructure needed, such as help desks, user manuals, and online resources.

- Risk Assessment

- Potential Risks: Identify potential risks associated with the technology implementation, including technical, financial, operational, and reputational risks.

- Mitigation Strategies: Consider strategies for mitigating these risks.

- Vendor Information (if applicable)

- Vendor Options: Research potential vendors or service providers, noting their reputation, service offerings, support and maintenance policies, and costs.

- Contractual Considerations: Understand the contractual terms and conditions, including customization options, scalability, and exit clauses.

Collecting this information will lay a solid foundation for completing the Technology Implementation Workbook. It ensures that you have a clear understanding of your organization’s needs, capabilities, and constraints, which is essential for planning and executing a successful technology implementation.

How can I assess my current technology infrastructure and identify areas for improvement?

Assessing your current technology infrastructure and identifying areas for improvement involves a systematic review of your hardware, software, network systems, and processes to ensure they meet your organization’s current and future needs efficiently and effectively. Here’s a structured approach to conduct this assessment:

- Inventory of Current Technology Assets

- Catalogue Hardware: List all hardware devices (servers, computers, mobile devices, etc.), noting their age, performance, and any issues or limitations.

- Software Audit: Inventory all software applications, including operating systems, office productivity tools, accounting software, and any industry-specific applications, noting versions, usage, and any redundancies or gaps.

- Evaluate System Performance and Scalability

- Performance Metrics: Assess the performance of your IT systems, including speed, uptime, and error rates. Use tools and software to monitor performance over time.

- Scalability Analysis: Determine whether your current technology infrastructure can scale to meet future business growth or if it will require upgrades or replacements.

- Security and Compliance Review

- Security Assessment: Evaluate the security measures in place to protect against cyber threats, including firewalls, antivirus software, and encryption protocols. Identify any vulnerabilities or areas lacking protection.

- Compliance Check: Ensure that your technology systems comply with relevant industry regulations and standards (e.g., GDPR, HIPAA). Note any areas of non-compliance or risk.

- Data Management and Backup Systems

- Data Storage and Access: Review how data is stored, accessed, and managed within your organization. Identify any inefficiencies or potential improvements in data handling.

- Backup and Recovery: Assess the effectiveness of your data backup and recovery systems. Ensure that backups are performed regularly and that recovery procedures are in place and tested.

- User Feedback and Support Systems

- Collect User Feedback: Gather feedback from end-users about their experiences with the technology infrastructure, including any challenges they face or tools they feel are missing.

- Support System Evaluation: Review the effectiveness of your IT support systems, including help desk responsiveness, user satisfaction, and resolution times.

- Integration and Interoperability

- System Integration Review: Assess how well different technology systems and applications integrate with each other. Identify any silos or integration challenges that may hinder workflow efficiency.

- Interoperability Analysis: Evaluate the interoperability of your systems, especially if you use technology from multiple vendors or platforms. Determine if there are any compatibility issues or opportunities for better integration.

- Cost Analysis

- Technology Costs: Review the costs associated with maintaining your current technology infrastructure, including hardware, software licenses, support contracts, and energy consumption.

- ROI Assessment: Assess the return on investment (ROI) of your technology assets. Consider whether reallocating resources or investing in new technologies could yield better results.

- Compile a Report and Develop an Action Plan

- Summary Report: Compile the findings of your assessment into a comprehensive report that highlights strengths, weaknesses, opportunities, and threats.

- Action Plan: Develop a prioritized action plan based on the assessment findings. This plan should address immediate needs, long-term improvements, and any strategic investments required to support your organization’s goals.

- Consult with Stakeholders

- Engage Stakeholders: Discuss the assessment findings and proposed action plan with key stakeholders, including IT staff, management, and end-users, to gain their insights and buy-in.

By systematically assessing your current technology infrastructure and identifying areas for improvement, you can make informed decisions that enhance efficiency, reduce risks, and support your organization’s strategic objectives.

What factors should I consider when selecting new technology tools for my firm?

Selecting new technology tools for your firm involves a comprehensive evaluation of various factors to ensure the chosen technology aligns with your business objectives, enhances operational efficiency, and offers scalability for future growth. Here are critical factors to consider:

- Business Needs and Objectives

- Strategic Alignment: Ensure the technology aligns with your firm’s strategic goals and addresses specific business needs or challenges.

- Problem Solving: Identify the key problems or inefficiencies you aim to solve with the new technology. Ensure the tool offers solutions that meet these needs.

- Functionality and Features

- Core Features: Assess whether the technology has the essential features required to meet your needs. Avoid paying for unnecessary features that won’t be utilized.

- Usability: Consider the user interface and ease of use. The technology should be intuitive for your team to adopt and use effectively.

- Integration Capabilities

- Compatibility: Check the compatibility of the new technology with your existing systems. Seamless integration is crucial to avoid operational disruptions.

- Data Migration: Understand the process for migrating existing data to the new system. Ensure the technology can handle this process smoothly.

- Scalability and Flexibility

- Growth Accommodation: Select technology that can scale with your firm’s growth. Consider whether it can handle increased loads or the addition of new users without significant upgrades.

- Customization: Assess the tool’s flexibility in terms of customization. It should accommodate your firm’s unique processes and workflows.

- Security and Compliance

- Data Security: Ensure the technology offers robust security features to protect sensitive information, including encryption and access controls.

- Regulatory Compliance: Verify that the technology complies with relevant industry regulations and standards, especially if you handle sensitive client data.

- Cost and ROI

- Total Cost of Ownership: Evaluate the total cost, including initial purchase, implementation, training, maintenance, and any recurring subscriptions.

- Return on Investment: Consider the potential ROI the technology could bring through increased efficiency, reduced costs, or improved client satisfaction.

- Vendor Reputation and Support

- Vendor Stability: Research the vendor’s stability and reputation in the market. A well-established vendor is likely to offer reliable technology and ongoing support.

- Support and Maintenance: Look into the vendor’s support services, including availability, responsiveness, and the presence of a knowledge base or community forums.

- Training and Support

- Learning Curve: Assess the learning curve associated with the new technology and the training resources available to help your team become proficient.

- Ongoing Support: Ensure that ongoing support is available to address any future issues or questions that arise.

- Trial and Feedback

- Free Trials or Demos: Whenever possible, use free trials or demos to test the technology’s functionality and suitability for your needs.

- User Feedback: Collect feedback from potential end-users during the trial period to gauge ease of use and satisfaction.

- Reviews and References

- Peer Reviews: Look for reviews or case studies from other firms or users who have implemented the technology. Their experiences can provide valuable insights.

- Reference Check: Ask the vendor for references from current clients, particularly those with similar use cases or business sizes as yours, to understand their experiences.

By thoroughly evaluating these factors, you can make an informed decision when selecting new technology tools, ensuring they contribute positively to your firm’s efficiency, security, and overall success.

How do I prioritize technology investments based on my firm’s budget and goals?

Prioritizing technology investments effectively requires a strategic approach that aligns with your firm’s budgetary constraints and overarching goals. Here’s a structured method to navigate this process:

- Align with Strategic Goals

- Identify Key Objectives: Begin by identifying your firm’s strategic goals and objectives. Determine which areas of your business could benefit most from technological enhancements.

- Impact Analysis: Assess how potential technology investments align with these goals. Prioritize technologies that directly support your strategic objectives, such as improving operational efficiency, enhancing client service, or expanding service offerings.

- Assess Current Technology Infrastructure

- Conduct a Technology Audit: Evaluate your current technology infrastructure to identify gaps, inefficiencies, and areas at risk of becoming obsolete. This assessment helps in pinpointing investments that are necessary versus nice to have.

- Determine Integration Needs: Consider how new technology will integrate with existing systems. Prioritize investments in technologies that seamlessly integrate, reducing the need for additional upgrades or replacements.

- Evaluate Cost Versus Value

- Total Cost of Ownership (TCO): For each potential technology investment, calculate the TCO, including initial purchase or subscription costs, implementation expenses, training, and ongoing maintenance.

- Return on Investment (ROI): Estimate the ROI for each technology investment. Prioritize those offering a higher ROI, which may include cost savings, increased revenue, improved client satisfaction, or competitive advantages.

- Assess Risk and Compliance

- Risk Assessment: Identify any risks associated with implementing new technology, including security vulnerabilities, data privacy concerns, and potential disruptions to operations. Prioritize investments that mitigate significant risks.

- Regulatory Compliance: Ensure that technology investments comply with industry regulations and standards. Prioritize investments that help maintain or achieve compliance.

- Consider Scalability and Flexibility

- Future-Proofing: Evaluate whether the technology can scale with your firm’s growth and adapt to future changes in the industry. Investments in scalable and flexible solutions should be prioritized to ensure long-term viability.

- Gather Stakeholder Input

- Involve Key Stakeholders: Include input from various stakeholders, including IT staff, end-users, and management, to ensure the selected technology meets the needs and expectations across the firm.

- Client Considerations: Consider the impact of technology investments on your clients. Prioritize investments that enhance client service, security, and access to information.

- Create a Prioritized Technology Roadmap

- Develop a Roadmap: Based on the evaluations, develop a technology investment roadmap that outlines priority projects, timelines, and budget allocations.

- Flexibility: Ensure the roadmap allows for flexibility to adjust priorities based on changing goals, market conditions, or financial constraints.

- Monitor and Review

- Regular Reviews: Regularly review the technology roadmap and priorities in light of new developments, feedback from implementation, and shifts in strategic goals or budgetary constraints.

- Performance Metrics: Establish metrics to monitor the performance and impact of technology investments. Use these insights to inform future investment decisions.

By systematically assessing how technology investments align with your firm’s strategic goals, evaluating their cost versus value, and considering scalability, risks, and stakeholder input, you can make informed decisions that maximize the impact of your technology budget and support your firm’s long-term success.

What are the best strategies for implementing new technology solutions in my firm?

Implementing new technology solutions in your firm successfully involves careful planning, clear communication, and strategic execution. Here’s a comprehensive approach to ensure effective implementation:

- Strategic Alignment

- Align with Business Goals: Ensure the new technology aligns with your firm’s strategic objectives. Clearly understand how this technology will support your business goals, such as improving efficiency, enhancing service quality, or expanding service offerings.

- Stakeholder Engagement

- Identify Stakeholders: Identify all stakeholders affected by the new technology, including team members who will use the technology, clients who may be impacted, and IT staff responsible for the deployment.

- Gather Input: Engage stakeholders early in the process to gather their input, expectations, and concerns. This helps in tailoring the implementation to meet the needs of all parties involved.

- Comprehensive Planning

- Develop an Implementation Plan: Create a detailed plan outlining the steps, timelines, responsibilities, and resources required for the implementation. This plan should include milestones for measuring progress.

- Risk Management: Identify potential risks associated with the implementation and develop mitigation strategies. This could include technical issues, user resistance, or data migration challenges.

- Effective Communication

- Communication Strategy: Develop a communication strategy that keeps all stakeholders informed throughout the process. This should include the reasons for the change, benefits of the new technology, and how it will impact various stakeholders.

- Feedback Channels: Establish channels for stakeholders to provide feedback and raise concerns during the implementation process.

- Training and Support