- Market Research: How Samera Does It

- Overview of the Accounting Industry

- Strategic Planning for Growth

- Current State of the Accounting Industry

- 5 Key Trends Shaping the Accounting Industry

- Making Your Accounting Firm Adaptable for Success and Stability

- Mapping the Growth Blueprint Amidst Disruption

- Conducting a Market Analysis for Your Accounting Firm

- Conclusion: Navigating Growth in the Current Accounting Landscape

- Using the Market Research Template

- Download the Market Analysis Workbook

The accounting industry is changing fast, and this change is affected by not one but multiple factors. If you are someone who runs an accounting practice, it is pretty sure that you must be thinking, “how do I ensure growth and continuity for my accounting business?” Well, this is what Samera’s Grow Your Accountancy course is targeted at. Our decades of experience, people, and market analysis has helped us sustainably grow in the accounting space. And now, with this course, we are here to help you build your own Unstoppable accountancy firm!

Welcome to the course’s first module, “Understanding the Accounting Firm Market,” where we explore the basics of how the accounting industry operates in today’s world. In this module, we’ll look at important aspects such as market trends, competition, client needs, technology, and regulations.

Whether you’re new to accounting or have been in the field for a while, this course is here to give you practical insights. We’ll break down the essentials of understanding the market—what makes it tick, who your competitors are, what clients are looking for, and how technology and rules affect your work.

Our goal is to provide you with real-world business acumen that you can turn into action. Join us as we navigate the ins and outs of the accounting industry’s market dynamics, helping you make better decisions in a business world that’s always changing.

Key Takeaways

- Understand Global Changes: The accounting industry is changing fast – technology, regulations, and client needs are shifting. You need to stay up-to-date to make sure you don’t get left behind.

- Build a Strategic Growth Plan: Use market analysis to identify opportunities and challenges, then create a growth plan based on your findings.

- Key Industry Trends: Tools like AI, cloud accounting, and cybersecurity aren’t optional anymore – they’re essential for growing your accountancy firm.

- Research Your Market: Find out what your clients are looking for and what your competitors are offering to find your USP and tailor your services.

Market Research: How Samera Does It

Let’s take a look at how Samera does it. In this episode of the Unstoppable podcast, Arun and Chris discuss how we have used market research and analysis to develop and inform our business strategy. From Arun first deciding on the UK healthcare niche to building a global outsourcing and support firm, this is how we use market research at Samera.

The Unstoppable Podcast

24th July 2024

Overview of the Accounting Industry

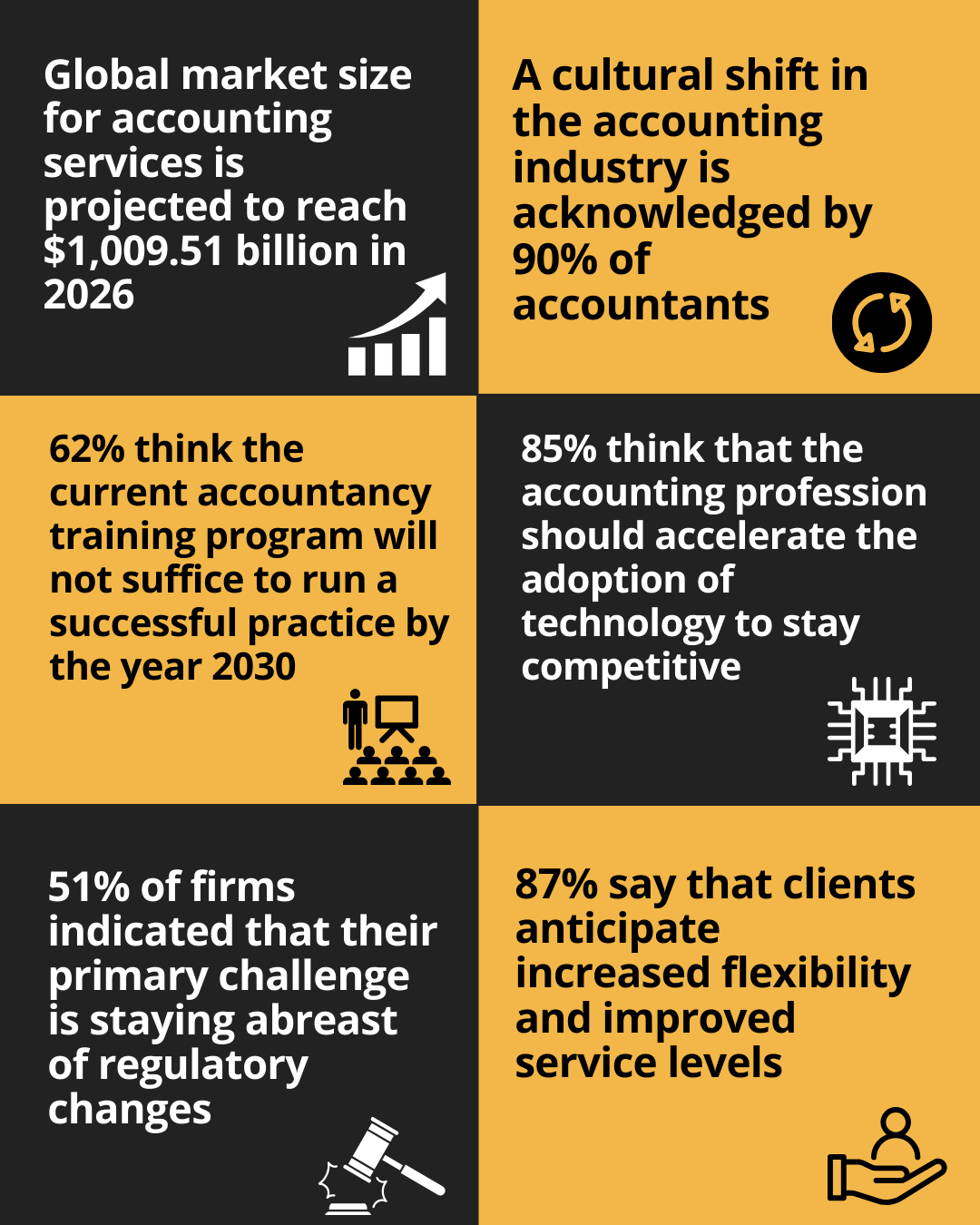

The accounting industry is always changing and this change is motivated by growth. Research suggests, the anticipated global market size for accounting services is projected to reach $735.94 billion by the year 2025 [1]. To succeed, you need to understand these changes and go with the flow. This chapter will explain why it’s crucial to keep up with what’s happening and how you can plan for your firm’s growth.

Click here to read our full report on the UK Accounting Industry.

How the Economy Affects Your Accountancy Firm

Constant Changes in the Accounting World

Imagine the accounting industry as a puzzle that keeps getting new pieces. To get a sense of change is pervading the industry, take this – a cultural shift in the accounting industry is acknowledged by 90% of accountants globally [2].

Laws change, technology evolves, and the way people do business shifts. If you want your firm to do well, you must pay attention to these changes.

Here are 5 key changes that have happened in the accounting industry in the last 5-7 years:

- Digital Transformation: The accounting industry has witnessed a significant shift towards digital transformation. Automation tools, cloud-based accounting software, and advanced data analytics have become integral, streamlining processes and improving efficiency.

- Increased Emphasis on Cybersecurity: With the rise in digital practices, there has been a heightened focus on cybersecurity. Accounting firms are increasingly investing in robust cybersecurity measures to protect sensitive financial information from cyber threats and data breaches.

- Remote Work Adoption: The events of the last few years, particularly the global pandemic, have accelerated the adoption of remote work in the accounting industry. Firms have embraced virtual collaboration tools and cloud-based solutions to facilitate remote work and maintain operational continuity.

- Evolution of Regulatory Landscape: The regulatory environment for accounting has evolved. Changes in tax laws, reporting requirements, and compliance standards have necessitated adjustments in accounting practices. Staying abreast of these regulatory shifts is crucial for firms to ensure compliance and avoid penalties.

- Rise of Client Expectations for Real-Time Insights: Clients now expect more than just year-end financial reports. There is a growing demand for real-time insights and proactive advisory services. Accounting firms are adapting by leveraging technology to provide clients with up-to-date financial information and strategic guidance throughout the year.

We will discuss each of above in much more depth later in this article.

Why Adaptation is Key

Staying stuck in old ways can make your firm struggle. Did you know, that Wolters Kluwer’s Survey of Tax and Accounting Professionals reports, over half of the surveyed companies encountered difficulties in staying updated with legislative changes [3].

In the accounting world, adaptation refers to the ability of firms to adjust and respond effectively to the dynamic changes in the industry. It involves staying relevant and resilient in the face of technological advancements, shifts in client expectations, and evolving regulatory landscapes. Adapting in the accounting context means embracing change proactively, ensuring that the firm remains competitive, efficient, and capable of meeting the evolving needs of clients.

Strategic Planning for Growth

Now, let’s talk about planning for growth. This doesn’t mean just hoping your firm gets bigger. It means thinking smart about where the industry is going and positioning your firm to go there too.

Here are 3 strategies your firm can implement to ensure sustainable growth:

- Diversification of Services: Expand service offerings to meet the evolving needs of clients. This could involve diversifying into advisory services, forensic accounting, or specialized industry expertise. By providing a broader range of services, accounting firms can attract new clients and deepen relationships with existing ones, fostering overall business growth.

- Strategic Technology Adoption: Implement advanced technologies to enhance efficiency and service delivery. This includes adopting automation tools, artificial intelligence, and data analytics. Technology not only streamlines internal processes but also allows firms to offer innovative solutions to clients. Embracing cutting-edge technology positions the firm as forward-thinking and can attract clients seeking modern, tech-savvy partners.

- Client Relationship Management and Retention: Prioritize client relationships as a core element of growth. Focus on delivering exceptional client service, maintaining open communication, and understanding client needs. Satisfied clients are more likely to provide referrals and continue engaging the firm’s services, contributing significantly to sustained growth. Additionally, nurturing long-term relationships positions the firm as a trusted advisor, fostering client loyalty.

Implementing a combination of these strategies can contribute to the overall growth and success of accounting firms. Diversifying services, adopting strategic technology, and prioritizing client relationships align the firm with the dynamic nature of the industry, ensuring it remains competitive and capable of capitalizing on emerging opportunities.

Current State of the Accounting Industry

In this chapter, we’ll take a straightforward look at how things stand in the world of accounting right now. The industry is like a river—always moving and changing. Understanding its current state is essential for anyone navigating these waters.

We’ll explore recent shifts, trends, and factors shaping accounting today, providing you with a clear snapshot of where things are at this moment. So, let’s dive in and get a grasp of the present landscape in the accounting industry.

Evolution of the Accounting Industry

Over time, the accounting industry has evolved a lot. As a matter of fact, in 2023, the estimated value of the global accounting sector is forecasted to be $675.14 billion [4]. As businesses grew, so did the need for more sophisticated financial management. That’s when accounting evolved. It became not just about numbers but also understanding the financial health of businesses.

Technology played a big role in this evolution. Computers replaced handwritten ledgers, making calculations faster and reducing errors. The internet allowed for quick communication and data sharing. Now, accounting isn’t just about looking back at what happened; it’s about using data to make informed decisions for the future. The industry has shifted from being a historical record-keeper to a strategic partner, helping businesses navigate the complexities of today’s financial landscape.

To understand the overarching evolution of the accounting industry, we will be focusing on technological advancements, regulatory changes, and the change in client expectations. So, let’s get right into it!

Technological Advancement

Welcome to the part where we talk about how technology has changed the way accountants do their work. Sage reports, a significant majority, 85% of accountants, think that the accounting profession in their country should accelerate the adoption of technology to stay competitive on the international stage [5].

We’ll look at 4 important ways things have evolved. From using paper and pens to now using digital tools, the accounting world has come a long way. Let’s jump in and see how technology has transformed the way accountants work.

- Transition to Digital Accounting Software: The accounting industry has witnessed a fundamental shift from manual record-keeping to digital accounting software. Gone are the days of handwritten ledgers; now, sophisticated software platforms automate financial processes. This evolution has not only increased efficiency but also reduced the likelihood of errors, providing accountants with more accurate and timely data.

- Cloud-Based Solutions: The advent of cloud technology has revolutionized how accounting data is stored and accessed. Cloud-based solutions allow accountants to work collaboratively and access financial information from anywhere with an internet connection. This flexibility has been especially crucial in the context of remote work, enabling accounting professionals to seamlessly collaborate and serve clients regardless of physical location.

- Integration of Data Analytics: Technology has empowered accountants with the ability to analyze large datasets quickly and derive meaningful insights. Data analytics tools enable accounting firms to identify trends, make predictions, and offer valuable strategic advice to clients. This evolution from manual data processing to data-driven decision-making has transformed the role of accountants into proactive business advisors.

- Enhanced Security Measures: As the digital landscape expanded, so did the importance of cybersecurity in the accounting industry. Technological advancements have led to the implementation of robust security measures to protect sensitive financial data. Encryption, multi-factor authentication, and secure cloud storage have become standard practices, ensuring the confidentiality and integrity of financial information.

These technological advancements collectively reflect a significant transformation in the accounting industry, enhancing efficiency, collaboration, and the ability to provide strategic insights to clients. The industry’s embrace of these technologies has not only streamlined traditional accounting processes but has also positioned accountants as integral partners in navigating the complexities of modern financial landscapes.

Regulatory Changes

As per the 2022 Year Ahead Survey by Accounting Today, 51% of firms indicated that their primary challenge is staying abreast of regulatory changes [6]. In this section focused on regulatory changes, we’re going to explore 4 ways from how taxes work to new ways of reporting financial information, these rules affect how accountants keep things in order.

Here are 4 key changes that have transpired in the accounting industry:

- Updates in Tax Laws: Tax regulations are in a constant state of change. Recent years have seen significant updates in tax laws, impacting how businesses and individuals report income, claim deductions, and fulfill their tax obligations. Staying abreast of these changes is crucial for accounting firms to ensure accurate and compliant financial reporting.

- Shifts in Reporting Standards: International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) undergo periodic updates. Changes in reporting standards influence how financial information is presented, affecting the comparability of financial statements globally. Accounting firms must adapt to these shifts to maintain transparency and alignment with evolving standards.

- Increased Regulatory Scrutiny: Regulatory bodies are placing a greater emphasis on transparency, accountability, and preventing financial misconduct. This heightened scrutiny requires accounting firms to implement more robust internal controls, ethical practices, and anti-fraud measures to meet regulatory expectations and maintain the integrity of financial reporting.

- Emphasis on Data Protection and Privacy: With the growing concern over data breaches and privacy, there has been a surge in regulations governing the protection of sensitive financial information. Compliance with data protection laws, such as the General Data Protection Regulation (GDPR), is now a critical aspect of accounting practices. Firms must implement stringent measures to safeguard client data and ensure regulatory compliance.

These regulatory changes highlight the dynamic nature of the accounting industry. Adapting to shifts in tax laws, reporting standards, increased regulatory scrutiny, and data protection requirements is essential for accounting firms to uphold integrity, meet client expectations, and navigate the complex regulatory landscape.

Evolving Client Expectations

Now, let’s discuss about what clients expect from accountants. This part is all about how client expectations have changed in recent times. As per the 2020 Sage Practice of Now report, 87% concur that clients anticipate increased flexibility and improved service levels from accountants without a corresponding rise in their fees [7].

From wanting quick updates on their finances to desiring advice for business growth, clients are looking for a bit more than the traditional accounting services. Here are 4 ways client expectations have evolved over time:

- Demand for Real-Time Insights: Clients now expect more than just yearly financial reports. There’s a growing desire for real-time insights into their financial data. Accounting firms are increasingly pressured to provide up-to-date information, enabling clients to make informed decisions promptly.

- Focus on Advisory Services: Beyond traditional bookkeeping and compliance, clients seek advisory services. They want accountants to not only manage their finances but also offer strategic guidance for business growth. The shift toward advisory roles requires accountants to possess a broader skill set, encompassing financial analysis and business consultation.

- Emphasis on Technological Integration: Clients expect accounting firms to leverage technology for efficiency and convenience. Online portals, mobile apps, and automated processes are now part of client expectations. Firms that integrate technology seamlessly into their services meet client demands for accessibility and streamlined interactions.

- Personalization of Services: Clients increasingly value personalized services tailored to their specific needs. One-size-fits-all approaches are no longer sufficient. Accounting firms must understand each client’s unique challenges and goals, adapting their services to provide targeted solutions. This personalized approach enhances client satisfaction and strengthens long-term partnerships.

These shifts in client expectations reflect a broader trend toward more dynamic and collaborative relationships between clients and accounting firms. Adapting to these expectations is crucial for firms looking to not only meet but exceed client needs in an ever-evolving business environment.

Digital Transformation in the Accounting Industry

To gain a full understanding of how the accounting industry has evolved, it’s important to make sense of the digital transformation that has changed the way accountants do their everyday tasks. Research indicates, currently 90% of small firms and 94% of large firms are seeking technological assistance to enhance their tax season performance [8]. This part is about the impact of digital transformation on traditional accounting practices.

We’ll look at five key ways things have changed. From automating repetitive tasks to using smart tools that analyze data, technology is reshaping how accountants work.

- Automation of Repetitive Tasks: Digital transformation has automated many routine accounting tasks. Mundane activities like data entry and transaction processing, once done manually, are now efficiently handled by accounting software. This not only reduces the risk of errors but also allows accountants to focus on more analytical and value-added aspects of their work.

- Cloud-Based Collaboration: The advent of cloud technology has transformed how accountants collaborate and share information. Cloud-based platforms enable real-time collaboration among team members and provide secure access to financial data from anywhere with an internet connection. This has been particularly impactful in the context of remote work, enhancing flexibility and efficiency.

- Data Analytics for Informed Decision-Making: Digital tools have introduced robust data analytics capabilities to the accounting realm. Accountants can now analyze large datasets quickly and extract meaningful insights. This shift from manual data processing to data-driven decision-making empowers accountants to offer more strategic guidance to clients, contributing to informed business decisions.

- Enhanced Security Measures: As digital practices became more prevalent, the need for heightened cybersecurity measures increased. The digital transformation of accounting has necessitated the implementation of advanced security protocols to protect sensitive financial information. Encryption, multi-factor authentication, and secure cloud storage are now standard practices to ensure data integrity and client confidentiality.

- Rise of Artificial Intelligence (AI): Artificial Intelligence has found its way into accounting processes, further accelerating digital transformation. AI-powered tools can analyze patterns, predict financial trends, and automate complex tasks. This enables accountants to provide more advanced insights and strategic recommendations to clients, marking a shift from traditional number-crunching to a more advisory role.

The impact of digital transformation on traditional accounting practices is profound, streamlining operations, enhancing collaboration, and elevating the role of accountants in providing strategic value to businesses. As the digital landscape continues to evolve, accounting professionals must embrace these changes to stay competitive and relevant in the ever-evolving industry landscape.

5 Key Trends Shaping the Accounting Industry

Let’s dive into the important changes happening in the accounting world. This section is all about five key trends shaping how accountants do their work. From using smart tools to handle routine tasks to keeping financial data safe online, these trends are reshaping the way things work.

We’ll explore each trend in detail, looking at how they impact the world of accounting. So here are all the significant trends that professionals need to know to stay up-to-date in the evolving field of financial management.

Building an Accountancy firm in an AI Age

Automation in Accounting

Automation is a significant trend transforming routine accounting tasks. In a recent study, 45% of accounting professionals expressed their intention to automate tedious and time-consuming accounting tasks, including tasks like data entry [9]. Software solutions now handle data entry, transaction processing, and reconciliation, reducing manual errors and enhancing efficiency. This shift allows accountants to focus on higher-value activities such as financial analysis and strategic decision-making.

Cloud Accounting Solutions

Cloud technology has revolutionized how accounting data is stored and accessed. Numbers reveal, cloud accounting is favored by 67% of accountants, with the belief that the adoption of cloud technology contributes to the enhanced success of their businesses [10]. Cloud accounting solutions provide secure, real-time access to financial information from anywhere with an internet connection. This flexibility facilitates collaborative work among team members, supports remote work structures, and ensures data availability without the constraints of physical locations.

Cybersecurity in Financial Data Management

With the increasing reliance on digital platforms, cybersecurity has become a paramount concern. Protecting financial data from cyber threats is crucial, prompting accounting firms to implement robust security measures. Encryption, multi-factor authentication, and secure cloud storage are standard practices, safeguarding sensitive information and maintaining client trust.

Niche Specializations

Accounting firms are increasingly adopting niche specializations to cater to specific industries or unique client needs. Sage reports that over 50% accountants are of the opinion that accountants entering the profession today should possess financial business advisory skills, including expertise in areas such as cash flow and growth modeling [11]. Specialized expertise allows firms to deliver tailored solutions, becoming trusted advisors in specialized domains. This trend emphasizes the importance of understanding industry intricacies and providing targeted services.

Data Analytics for Strategic Insights

The integration of data analytics tools is transforming how accountants derive insights from financial data. Analytics enables accountants to analyze large datasets quickly, identify patterns, and make informed predictions. This shift from traditional reporting to data-driven decision-making positions accountants as strategic partners, offering valuable insights for client business growth.

Understanding and adapting to these trends is paramount for accounting professionals aiming to stay relevant and competitive. The 5 trends mentioned above will collectively shape the future of the accounting industry, influencing how financial information is managed, analyzed, and leveraged for strategic advantage.

But now that you’re informed about these trends, is your firm ready to adapt for the changes that will be brought forward? Let’s discuss that in the next chapter!

Making Your Accounting Firm Adaptable for Success and Stability

This chapter is all about adapting to changes in the accounting world. We’ll look at three important things: using new tools and methods, making sure your team keeps learning, and managing client relationships well in our tech-driven age. Let’s explore these strategies to help your firm stay steady and successful in the ever-changing world of accounting.

Strategies for Integrating New Technologies and Practices:

Embracing new technologies is like updating your toolkit to work more efficiently. In fact, within the next three years, it is anticipated that 58% of accounting professionals will be employing artificial intelligence solutions to automate accounting tasks [12].

Start by adopting advanced accounting software that automates tasks like data entry and reconciliation. This not only reduces errors but also frees up time for more important work. Next, look into automation tools that can handle repetitive tasks, making processes smoother. Cloud-based solutions are also handy—they let you access financial data from anywhere, which is especially useful for remote work.

Creating a culture that welcomes these changes is crucial. Encourage your team to use these new tools and stay updated on the latest practices. Training programs and workshops can help everyone get comfortable with the changes. When everyone in your firm is on board with the latest technologies, your firm becomes more modern and efficient. It’s about using these tools smartly to make your work easier and more effective.

The Role of Professional Development and Continuous Learning:

Continuous learning is crucial in an industry shaped by rapid technological changes. Establishing a culture of professional development within your firm ensures that accountants stay updated on the latest trends, tools, and regulations. To spell out in numbers, technology is reported to assist with staff engagement and morale, which are crucial factors in retaining staff, by over 60% of large firms [13].

This may involve providing training programs, encouraging participation in industry events, and supporting certifications. A well-trained team not only adapts more effectively to industry shifts but also adds significant value to clients through informed decision-making. This is especially true when we heed to the fact that, nearly 62% of accounting professionals, concur that the current accountancy training program will not suffice to run a successful practice by the year 2030 [14].

When your team is continuously learning, they can adapt to changes in the industry more easily. This not only makes your firm more resilient but also helps your accountants provide better insights to clients. The goal is to create a culture where everyone values staying informed, contributing to the overall success of your firm. Continuous learning ensures your team is well-equipped to handle whatever comes their way in the ever-changing world of accounting.

Client Relationship Management in a Tech-Driven Era

As technology plays an increasing role in accounting, maintaining strong client relationships requires a delicate balance between efficiency and personalization. While digital tools enhance efficiency, it’s essential to preserve a personal touch in client interactions. Regular communication, understanding individual client needs, and offering personalized services contribute to client satisfaction. Implementing client relationship management (CRM) systems can streamline communication and help firms maintain personalized connections with clients in a tech-driven environment.

In fact, an overwhelming majority of 82% accounting firms, state that clients now anticipate a greater range of services and resources from accountants compared to five years ago [15]. Personalizing your services based on their requirements adds a human touch. While technology helps in managing large amounts of data, it’s the personal connection that makes clients feel valued. Striking this balance ensures that your firm remains efficient and modern without sacrificing the personal relationships that are the foundation of a successful accounting practice.

Mapping the Growth Blueprint Amidst Disruption

Let’s talk about how your accounting firm can grow even when things around you are changing. This part is about planning for growth in the accounting world. We’ll explore two important strategies: being flexible in how you do business and staying proactive in the face of new rules and technology. Join us as we dive into these approaches to help your firm not just adapt but thrive in the evolving world of accounting.

Emphasizing the Need for Flexible and Adaptive Business Models

To plan for growth, your firm must be adaptable, like a well-tuned instrument that can play different tunes. Embrace flexibility in your business model, allowing for adjustments as industry trends evolve. This involves regularly assessing the market, identifying emerging client needs, and tweaking your services accordingly. Being flexible means anticipating changes and quickly adapting to seize new opportunities.

Diversifying your service offerings is another facet of flexibility. Offering a range of services tailored to client demands positions your firm for growth. This may involve exploring niche specializations, expanding advisory services, or entering new markets. By tailoring your business model to changing demands, your firm becomes agile, resilient, and poised for sustained growth.

Encouraging Proactive Approaches to New Regulations and Technological Advancements

Proactivity is the cornerstone of growth planning, akin to steering the ship rather than merely following the current. Stay ahead of the curve by actively monitoring and adapting to new regulations. This involves not only ensuring compliance but also strategically leveraging regulatory changes to enhance service offerings. Understand how new regulations impact your clients and position your firm to provide valuable solutions.

Likewise, staying proactive in adopting technological advancements positions your firm as a leader rather than a follower. Regularly assess emerging technologies, evaluate their potential benefits, and integrate them strategically into your operations. Embrace automation, explore data analytics tools, and leverage new software to enhance efficiency and offer innovative services to clients.

Conducting a Market Analysis for Your Accounting Firm

To foster growth, a comprehensive market analysis is vital for understanding the current landscape and identifying areas of potential expansion. This chapter provides guidance on conducting a robust market analysis and emphasizes the importance of gauging your firm’s position in the evolving market.

Assessing the Current Market

Let’s look at how to figure out what’s happening in the market right now. This part is about assessing the current market for your accounting firm. We’ll explore five key areas to focus on. From understanding what your competitors are doing to knowing your clients’ needs, these steps will help you see where your firm stands and where it can grow.

Here are 5 key areas you need to look into to conduct a thorough market analysis.

- Competitor Analysis: Evaluate the strengths and weaknesses of competitors in your area. This involves understanding their service offerings, client base, and pricing strategies. Identify gaps in their services that your firm can potentially fill.

- Client Demographics and Needs: Understand the demographics of your current client base and identify emerging client needs. Analyze the industries you serve, the size of businesses, and specific challenges they face. This insight informs targeted service offerings.

- Regulatory Environment: Stay abreast of regulatory changes impacting the accounting industry. Assess how these changes affect your firm and clients. Anticipate shifts in compliance requirements and position your firm to provide relevant solutions.

- Technology Adoption in the Market: Analyze how other firms in your market are adopting technology. Assess the prevalence of cloud-based solutions, automation tools, and data analytics. Identify areas where your firm can leverage technology for a competitive edge.

- Client Satisfaction and Feedback: Gather client feedback and assess satisfaction levels. Understand what clients appreciate about your services and where improvements can be made. Satisfied clients are more likely to stay and refer others.

Understanding Your Firm’s Position

Now, let’s talk about figuring out where your accounting firm stands in the big picture. This part is about understanding your firm’s position. We’ll look at four key indicators to help you see how well your firm is doing in the market. From keeping your clients happy to making sure your team is stable, these indicators will give you a clear view of your firm’s position.

Below are 4 major indicators to recognize where your firm stands in the current market settings and also to benchmark future goals against:

- Client Retention Rates: Track how well your firm retains clients over time. High retention rates indicate satisfied clients and a strong foundation for growth.

- Market Share Growth: Monitor the growth of your firm’s market share compared to competitors. A steady increase in market share signals success in attracting new clients or expanding services.

- Employee Satisfaction and Retention: Gauge the satisfaction and retention of your team. A content and stable workforce contributes to the consistent delivery of quality services.

- Adaptability to Industry Trends: Assess how well your firm adapts to emerging industry trends. This includes the integration of new technologies, adoption of industry best practices, and flexibility in service offerings.

Understanding your market and firm position provides a foundation for strategic decision-making. By conducting a thorough market analysis and regularly assessing key indicators, your accounting firm can identify growth opportunities and navigate the evolving industry landscape with confidence.

Conclusion: Navigating Growth in the Current Accounting Landscape

In the accounting world, just like in any other walk of business, adapting and growing are not just strategies but necessities for sustained success. We’ve explored key insights on how to position your accounting firm for growth, emphasizing the importance of flexibility, proactive approaches, and strategic planning.

Here is a quick rundown of all that we have covered in this article from the current state of accounting to the rends shaping up the future:

Key Insights

- Flexibility is Key: Embrace flexible business models that allow for adjustments based on industry trends and client needs. Adaptability ensures your firm can seize emerging opportunities.

- Proactivity Drives Success: Stay proactive in understanding and implementing new regulations and technological advancements. Being ahead of the curve positions your firm as a leader in the industry.

- Client Understanding is Crucial: Regularly analyze the market to understand client demographics, needs, and satisfaction levels. Client-centric approaches are foundational to growth.

- Assess Your Firm’s Position: Regularly evaluate key indicators like client retention rates, market share growth, employee satisfaction, and adaptability to industry trends. This provides a clear picture of your firm’s position.

Using the Market Research Template

To practically implement these insights, we encourage you to utilize the Market Analysis Template provided. This template serves as a strategic tool, guiding you through the process of assessing the current market, understanding your firm’s position, and identifying growth opportunities. By systematically filling in the details, you can create a roadmap for your firm’s growth tailored to the evolving accounting landscape.

Takeaways for Maintaining Agility and Foresight:

- Embrace Change Proactively: View change not as a challenge but as an opportunity. Proactively embrace new technologies, regulations, and market shifts to stay ahead.

- Invest in Continuous Learning: Prioritize professional development for your team. Continuous learning ensures that your firm’s skill set remains relevant and adaptable to industry changes.

- Cultivate a Client-Centric Culture: Understand and respond to client needs promptly. A client-centric approach fosters loyalty and positions your firm as a trusted advisor in an evolving market.

- Regularly Review and Adjust Strategies: Periodically revisit your firm’s strategies. Regular reviews and adjustments keep your business agile and responsive to emerging trends.

- Foster a Culture of Innovation: Encourage a culture that values innovation. This includes adopting new technologies, exploring niche specializations, and finding creative solutions to client challenges.

In sum, navigating growth in the contemporary accounting landscape demands a proactive and strategic approach. By combining flexibility, client understanding, and a commitment to continuous improvement, your firm can not only adapt to changes but thrive in an ever-evolving industry. Utilize the insights and tools provided to embark on a journey of strategic growth and long-term success for your accounting firm.

Download the Market Analysis Workbook

Download our Market Analysis Template below and start the process of developing your own growth action plan for your accounting firm.

By using the information in this module, as well as your own research, you will be able to draw a clearer picture of the market trends that will affect your firm’s growth, as well as strategies to overcome them. You will also learn more about your competitors to research techniques and strategies that you can replicate. Lastly, you’ll develop a template for the kind of clients, industries and niches you will target.

By putting these together, you’ll gain a better understanding of how, when and why you will be implementing the techniques you learn in this course.

Download the Market Analysis Workbook:

Help to Fill in the Market Analysis Workbook

How do I begin filling out the market analysis template?

To begin filling out the market analysis template, follow these structured steps to ensure a comprehensive understanding and analysis of your market:

- Gather Preliminary Information: Start by collecting basic data about your industry, including size, growth rates, and trends. Sources might include industry reports, market research studies, and financial news related to your sector.

- Identify Your Objective: Clearly define what you aim to achieve with the market analysis. Whether it’s understanding customer needs, identifying competition, or spotting market trends, having a clear objective will guide your research and analysis.

- Segment Your Market: Break down the broader market into smaller segments based on various criteria like demographics, geographics, psychographics, and behavioristics. This will help you to target your analysis more effectively.

- Research Your Market: Delve into each segment to understand the dynamics, including customer needs, purchasing habits, and preferences. Use surveys, interviews, and public databases to gather information.

- Analyze the Competition: Identify your main competitors and analyze their strengths, weaknesses, market share, and positioning. This will help you to position your firm more strategically.

- Understand Legal and Economic Conditions: Take into account any regulatory, legal, or economic factors that could impact your market or business operations.

- Fill in the Template: Start inputting your gathered data into the market analysis template. Be thorough and precise, ensuring each section is filled out based on the insights you’ve gathered.

- Review and Refine: Once you’ve filled out the template, review the information for accuracy and completeness. Refine your analysis where necessary, and consider getting feedback from colleagues or industry experts.

- Draw Conclusions and Plan Actions: Based on your completed market analysis, draw conclusions about your market positioning, opportunities, and threats. Use these insights to plan strategic actions that align with your business goals.

- Regular Updates: Markets are dynamic, so make a schedule to regularly update your market analysis to keep it relevant. This could be annually or in response to significant market changes.

Starting with a methodical approach will make the process of filling out the market analysis template more manageable and will lead to more insightful and actionable conclusions.

How can I identify and analyze current trends in the accounting industry that affect my firm?

Identifying and analyzing current trends in the accounting industry that affect your firm involves several steps, incorporating both research and practical evaluation of your firm’s position within the industry. Here’s a guide to help you through the process:

- Industry Reports and Market Analysis

- Subscribe to Industry Publications: Journals, magazines, and newsletters focused on accounting and finance can provide insights into emerging trends, regulations, and technologies.

- Market Research Reports: Purchase or access market research reports from firms like Gartner, Forrester, or specific accounting industry analysts. These reports often contain detailed analyses of market trends, future outlooks, and statistical data.

- Regulatory and Legislative Changes

- Government Websites and Publications: Keep an eye on government and regulatory body websites for any changes in accounting standards, tax laws, and compliance requirements. For example, changes in GAAP, IFRS, or tax regulations can significantly impact your practices.

- Consult with Legal and Compliance Experts: Sometimes, the implications of new laws or standards are not entirely clear. Consulting with experts can provide clarity and proactive strategies to address these changes.

- Technological Advancements

- Technology News and Conferences: Stay updated on new accounting software, AI and machine learning developments, blockchain, and other technologies affecting the accounting sector. Attending tech conferences or webinars can also offer insights and networking opportunities.

- Adopt and Adapt: Evaluate how new technologies can be integrated into your existing systems. Consider pilot programs or small-scale implementations to test these technologies’ effectiveness.

- Professional Networking

- Join Professional Associations: Organizations like the American Institute of CPAs (AICPA) or the Association of Chartered Certified Accountants (ACCA) offer resources, forums, and events that can keep you informed about industry trends.

- Networking Events and Conferences: Attend industry conferences, workshops, and seminars. These are excellent opportunities to learn from peers, share experiences, and identify emerging trends.

- Customer and Client Feedback

- Surveys and Feedback Forms: Regular feedback from your clients can provide direct insights into what services are in demand, their satisfaction with your current offerings, and areas for improvement or innovation.

- Market Demand Analysis: Analyze the demand for different accounting services. Look for patterns in requests from clients or inquiries from potential clients to identify new market opportunities.

- Competitor Analysis

- Monitor Competitors: Keep an eye on your competitors’ offerings, marketing strategies, and client engagements. This can offer clues to industry shifts and help you position your firm strategically.

- SWOT Analysis: Perform a Strengths, Weaknesses, Opportunities, and Threats (SWOT) analysis comparing your firm with competitors. This can help identify strategic areas for development or differentiation.

- Continuous Learning and Development

- Professional Development: Encourage continuous learning within your firm. This can be through online courses, workshops, or certifications in emerging areas like cyber security, data analytics, or sustainable accounting.

- Internal Knowledge Sharing: Foster a culture of knowledge sharing within your firm. Regular meetings, workshops, or internal newsletters can help disseminate new information and insights among your team.

By following these steps, you can effectively identify and analyze current trends in the accounting industry that might affect your firm. It’s crucial to remain agile and open to change, as the industry is continuously evolving with advancements in technology, regulations, and global economic shifts.

How do I determine the potential size of my target market in the market size and potential section?

Determining the potential size of your target market is a critical step in understanding the opportunity for your product or service. This process involves a combination of market research, analysis, and forecasting. Here’s a structured approach to help you estimate the potential size of your target market in the “Market Size and Potential” section of your business plan or market analysis report:

- Define Your Target Market

- Segmentation: Break down the market into segments based on demographics (age, gender, income level), geographics (location), psychographics (lifestyle, values), and behavior (purchasing habits).

- Target Market Characteristics: Clearly define the characteristics of your potential customers within these segments. Who are they? What are the needs or problems that your product or service solves?

- Choose Your Market Sizing Method

- There are three primary methods to estimate market size:

- Top-Down Approach: Start with the overall market size and then narrow down to your target segment using available industry reports, market research, and statistical data.

- Bottom-Up Approach: Calculate potential market size starting from individual consumer demand within your target market and scale up. This often involves more direct market research and can be more accurate but time-consuming.

- Value Chain Analysis: Assess the size and potential of your market by examining the value chain of your industry, identifying where your product or service fits, and estimating the value added at each step.

- Conduct Market Research

- Primary Research: Directly gather information from potential customers through surveys, interviews, focus groups, or experiments. This can provide insights into customer needs, willingness to pay, and the potential customer base size.

- Secondary Research: Utilize existing research, industry reports, government databases, academic papers, and any relevant publications that can provide data on your target market’s size and potential growth.

- Analyze Competitors

- Market Share and Saturation: Look at the number of competitors and their market share to understand the saturation level in the market. High saturation might indicate a smaller available market size, while few competitors might suggest a larger opportunity.

- Gaps and Opportunities: Identify any gaps in the offerings of your competitors where your product or service can stand out or fulfill an unmet need.

- Estimate Market Size

- Calculations: Use the data gathered to estimate your market size. For the top-down approach, apply percentages based on your research to the broader market figures. For the bottom-up approach, multiply your potential customer base by the estimated average revenue per customer.

- Adjust for Growth and Trends: Consider historical growth rates and future trends that could affect the market size. Adjust your estimates accordingly to reflect these dynamics.

- Validate and Refine

- Feedback and Expert Insights: Present your findings to mentors, industry experts, or potential customers to validate your assumptions and refine your estimates.

- Continuous Monitoring: Market sizes and potentials are not static. Continuously monitor market trends, customer feedback, and competitive landscape to adjust your estimates.

- Document Your Findings

- Clear Assumptions: Document all assumptions made during your estimation process. This adds credibility to your analysis and helps stakeholders understand the basis of your market size estimation.

- Sources and Methodology: Include a detailed description of your research methodology and sources of data. This transparency can increase the confidence in your findings.

By systematically following these steps, you can effectively determine the potential size of your target market, providing you with valuable insights for strategic planning, investment decisions, and marketing strategies. Remember, the accuracy of your market size estimation greatly depends on the quality of your research and the validity of your assumptions.

Should I include a SWOT analysis in my market analysis, and if so, how do I approach it?

It offers a comprehensive view of the Strengths, Weaknesses, Opportunities, and Threats related to your business within the context of the wider market. A SWOT analysis helps in strategic planning by translating insights into actions that align with your business objectives. Here’s how you can approach incorporating a SWOT analysis into your market analysis:

- Understand the Purpose of SWOT in Market Analysis

- Strengths and Weaknesses: These are internal factors that affect your business. Strengths are assets and resources that you can leverage for competitive advantage, while weaknesses are areas that need improvement.

- Opportunities and Threats: These are external factors stemming from market dynamics, industry trends, economic shifts, and regulatory changes. Opportunities are external chances to improve your performance in the environment, and threats are external challenges caused by the market or competition.

- Conduct Thorough Market Research

- Before starting your SWOT analysis, gather comprehensive information about the market. This includes industry trends, competitor strategies, customer preferences, regulatory environment, and technological advancements. Use both primary and secondary research to collect data.

- Identify Your Strengths

- Look internally to identify what your business does well. This could include a strong brand, unique technology, customer loyalty, or an efficient supply chain.

- Consider strengths in relation to competitors. What do you do better than others in the market?

- Acknowledge Your Weaknesses

- Be honest about where your business could improve. Weaknesses might include limited resources, gaps in the product line, or areas where competitors have an edge.

- Think about weaknesses from both an internal perspective and in terms of your position in the market.

- Spot Opportunities

- Use your market research to identify potential opportunities. This could be an emerging need of your target customers, a gap in competitors’ offerings, or new markets opening due to technological changes or regulatory shifts.

- Think about how your strengths can be used to capture these opportunities.

- Assess Threats

- Look for potential threats in the market, such as new competitors, changing customer preferences, regulatory changes, or technological disruptions that could make your product or service less competitive or obsolete.

- Evaluate how your weaknesses may make you vulnerable to these threats.

- Develop Strategies

- For each element of the SWOT analysis, develop strategies that address how to:

- Leverage strengths to take advantage of opportunities.

- Overcome weaknesses to better capture opportunities.

- Use strengths to mitigate threats.

- Address weaknesses to avoid falling prey to threats.

- Integrate SWOT into Market Analysis

- Clearly present the SWOT analysis within your market analysis report. Show how the insights from SWOT directly inform your market entry strategies, product development, marketing strategies, and risk management.

- Highlight how your understanding of the SWOT factors will guide your business’s strategic decisions and positioning within the market.

- Review and Update Regularly

- Market conditions, competitor strategies, and internal capabilities change over time. Regularly review and update your SWOT analysis to reflect these changes and adjust your strategies accordingly.

Including a SWOT analysis in your market analysis not only provides a snapshot of where your business currently stands but also helps in plotting a strategic course forward. It’s an essential tool for aligning your business strategy with the realities of the market and positioning your business for success.

What are the key components I should focus on in the current market trends section?

In the “Current Market Trends” section of your analysis or business plan, focusing on key components that give insights into the market dynamics, consumer behaviors, technological advancements, and competitive landscape is essential. These components help in understanding the trajectory of the industry and how your business can align itself with, or capitalize on, these trends. Here are the key areas you should focus on:

- Consumer Behavior Trends

- Purchasing Patterns: Note any shifts in how, where, and why consumers are buying products or services in your industry. This might include changes in preferences towards online shopping, subscription models, or demand for sustainable and ethical products.

- Customer Preferences and Needs: Highlight changes in what customers value, such as increased interest in personalized experiences, convenience, or health and wellness products.

- Technological Advancements

- Emerging Technologies: Identify new technologies that are influencing your industry, such as AI, machine learning, blockchain, or IoT, and how they’re changing business operations, product offerings, or customer interactions.

- Adoption Rates: Discuss how quickly these technologies are being adopted within your industry and the potential impact on market dynamics.

- Regulatory Changes

- New Legislation: Any recent or upcoming legislative changes that could affect the market, such as privacy laws, environmental regulations, or industry-specific compliance requirements.

- Impact on the Industry: Analyze how these changes might influence market entry barriers, costs, or competition.

- Market Growth or Decline

- Growth Rates: Present current market growth rates and projections. Identify whether the market is expanding, stable, or declining, and the factors driving these trends.

- Market Saturation: Evaluate the level of market saturation. High saturation might indicate limited growth potential, whereas emerging markets may offer significant growth opportunities.

- Competitive Landscape

- Market Share Distribution: Discuss the distribution of market share among key players and whether the market is fragmented or dominated by a few entities.

- Competitive Strategies: Note any prevalent competitive strategies, such as pricing wars, innovation focus, mergers and acquisitions, or expansions into new markets.

- Economic Factors

- Macroeconomic Trends: Consider broader economic trends that could impact your industry, such as inflation rates, employment levels, and consumer spending power.

- Industry-specific Economic Indicators: Highlight any economic indicators particularly relevant to your industry, like commodity prices for the manufacturing sector or disposable income levels for luxury goods.

- Societal and Cultural Trends

- Shifts in Values and Lifestyles: Identify societal trends that could influence your market, such as increased health consciousness, remote work trends, or the desire for experiences over products.

- Demographic Changes: Discuss demographic shifts, such as aging populations or urbanization trends, and their potential impact on market demand.

- Environmental and Sustainability Trends

- Sustainability Focus: The growing consumer demand for sustainable and environmentally friendly products and practices.

- Regulatory Impact: How environmental regulations could shape industry practices and consumer expectations.

- Presenting the Trends

- When presenting these trends, it’s crucial to:

- Use Data to Support Claims: Incorporate relevant data and statistics to back up your observations about market trends.

- Analyze the Impact: Don’t just list trends; analyze their potential impact on your business and the industry at large.

- Visualize Information: Use charts, graphs, and infographics to make the data more accessible and engaging.

By thoroughly covering these components, you can provide a comprehensive overview of the current market trends that will inform strategic decision-making and help identify opportunities and challenges within your industry.

How can I effectively identify and analyze my competitors through the competitor analysis section?

Effectively identifying and analyzing your competitors in the competitor analysis section involves a systematic approach to gathering, reviewing, and interpreting data about your rivals. This process helps in understanding their strategies, strengths, weaknesses, and the overall competitive landscape. Here are steps and key elements to consider for a comprehensive competitor analysis:

- Identify Your Competitors

- Direct Competitors: These are businesses offering the same or similar products or services targeting the same market segment as you.

- Indirect Competitors: These competitors provide alternative solutions to the same problems your products or services address but may not operate in the exact same category.

- Potential Competitors: Keep an eye on companies not currently in your market but have the capability to enter.

- Gather Information

- Company Overview: Basic information such as size, location, and history.

- Product or Service Offerings: What they offer, their pricing strategy, and any unique features or benefits.

- Market Position: Their target market segments, market share, and positioning strategy.

- SWOT Analysis: Identify their strengths, weaknesses, opportunities, and threats based on available information.

- Analyze Their Marketing Strategies

- Online Presence and Digital Marketing: Analyze their website, search engine optimization (SEO) strategies, content marketing, and social media presence.

- Advertising and Promotional Tactics: Look into their advertising approaches, sponsorships, or other promotional activities.

- Sales Channels: Understand the channels through which they sell their products or services, including online platforms, retail distribution, direct sales, or partnerships.

- Evaluate Their Financial Performance

- Revenue and Profitability: If available, review their financial statements to understand their revenue, profitability, and growth trends.

- Funding and Investment: For startups or growth-stage companies, look at their funding history, investors, and investment rounds.

- Understand Their Operational Strengths and Weaknesses

- Supply Chain: Analyze the efficiency and reliability of their supply chain and logistics.

- Customer Service: Consider their customer service reputation, including reviews and feedback.

- Innovation and Product Development: Evaluate their capacity for innovation, research and development (R&D) initiatives, and product launch frequency.

- Study Their Workforce and Culture

- Employee Satisfaction: Look for information on their workforce size, culture, employee satisfaction, and turnover rates.

- Leadership: Understand their leadership team, their background, and leadership style.

- Tools and Resources for Competitor Analysis

- Websites and Company Reports: Start with their official website, annual reports, and press releases.

- Social Media and Content: Analyze their content and engagement on platforms like LinkedIn, Twitter, Facebook, and Instagram.

- Customer Reviews and Forums: Sites like Yelp, Trustpilot, and industry-specific forums can provide insights into customer experiences and perceptions.

- Market Research Reports: Access industry reports from firms like Gartner, IBISWorld, or Statista for broader market and competitor insights.

- Financial Databases: Use databases like Crunchbase, Bloomberg, or Hoovers for financial and corporate information on competitors.

- Analysis and Strategy Development

- Use the information gathered to benchmark your business against competitors on various parameters like product offerings, market share, marketing strategies, etc.

- Identify gaps in the market that competitors are not addressing, which could represent opportunities for your business.

- Develop strategies to leverage your strengths and address your weaknesses relative to competitors.

- Continuous Monitoring

- Competitor analysis is not a one-time task but an ongoing process. Markets, technologies, and consumer preferences change, and so do your competitors’ strategies. Set up a system for regularly updating your competitor analysis to stay informed and adapt your strategies accordingly.

- Incorporating these elements into your competitor analysis section will give you a clearer understanding of the competitive landscape, allowing you to make informed strategic decisions and identify areas where you can differentiate and excel.

What should I look for when assessing customer segmentation in the market analysis?

When assessing customer segmentation in the market analysis, your goal is to understand how the market can be divided into distinct groups with similar needs, preferences, or demographic profiles that might require unique products or marketing strategies. Effective customer segmentation allows you to tailor your offerings and communications to meet the specific needs of different market segments, maximizing efficiency and impact. Here are key aspects to focus on:

- Demographic Segmentation

- Age, Gender, and Family Structure: Different products and marketing messages appeal to different age groups, genders, and family compositions.

- Income and Occupation: People’s buying power and preferences often correlate with their income levels and occupations.

- Education and Social Class: Education level and social class can influence purchasing behaviors and preferences.

- Geographic Segmentation

- Location: Urban vs. rural areas can drastically affect consumer needs and access to products.

- Climate and Region: Geographic conditions can influence the demand for certain products or services.

- Psychographic Segmentation

- Lifestyle: People’s lifestyles, including activities, interests, and opinions, can influence their buying habits.

- Values and Attitudes: Personal values and attitudes towards various issues (e.g., environmental concern, health consciousness) can dictate consumer preferences for products and brands.

- Personality Traits: Personality characteristics can also play a role in the appeal of certain products or marketing strategies.

- Behavioral Segmentation

- Purchasing Behavior: Look at how different groups approach buying decisions, including factors like brand loyalty, usage rate, and sensitivity to price changes.

- Benefits Sought: Understand the primary benefits different segments seek in a product, such as a convenience, quality, or affordability.

- Engagement Level: Some segments may be more engaged with certain media channels or more receptive to interactive marketing efforts.

- Needs-Based Segmentation

- Identifying distinct needs within the market that your product or service can meet. This can often cross over with other segmentation criteria but focuses on the specific problem or desire that your offering addresses.

When Assessing Customer Segmentation, Consider:

- Market Research Data: Utilize both primary and secondary market research to gather data on potential customers. Surveys, focus groups, and analysis of market trends can provide insights into how to segment your market effectively.

- Competitor Strategies: Observe how competitors segment the market and their approaches to targeting different groups. This can reveal gaps in the market or opportunities for differentiation.

- Technological Tools: Use data analytics and customer relationship management (CRM) software to analyze customer data and identify patterns or segments within your existing customer base.

- Regulatory Environment: Be aware of any legal or regulatory considerations that may affect how you can use customer data or target certain segments.

Implementation in Market Analysis

- Clear Segment Definitions: Provide clear and concise definitions for each segment, including size, characteristics, and the criteria used for segmentation.

- Segment Attractiveness: Assess and document the attractiveness of each segment in terms of size, profitability, accessibility, and alignment with your business’s capabilities and goals.

- Target Segment Strategy: Based on your analysis, identify which segments are most attractive for your business to target. Outline strategies for targeting these segments through product differentiation, marketing messages, and distribution channels.

Customer segmentation in market analysis is about understanding the heterogeneous nature of the market and identifying pockets of opportunities where your business can uniquely meet customer needs. By focusing on these key aspects, you can develop targeted strategies that increase the effectiveness of your marketing efforts, product development, and overall business strategy.

Can you provide tips on how to gather reliable data for my market analysis?

Gathering reliable data for your market analysis is crucial to ensure the accuracy and credibility of your findings. Reliable data helps in making informed decisions, understanding market dynamics, and identifying opportunities and threats. Here are some tips on how to gather reliable data for your market analysis:

- Define Your Objectives

- Clearly define what information you need from your market analysis. This will guide your research process and help you stay focused on gathering relevant data.

- Use a Combination of Primary and Secondary Research

- Primary Research: Collect data directly from the source through surveys, interviews, focus groups, and observations. This data is original and specifically gathered for your analysis.

- Surveys and Questionnaires: Use online survey tools to reach a broad audience. Ensure questions are unbiased and cover a range of topics relevant to your market analysis.

- Interviews and Focus Groups: Conduct in-depth discussions with industry experts, potential customers, and other stakeholders to gather qualitative insights.

- Secondary Research: Utilize existing data from reliable sources. This includes industry reports, academic papers, government publications, and reputable news outlets.

- Industry Reports and Market Research: Look for reports from known market research firms like Nielsen, Gartner, or Forrester. These can provide comprehensive market insights and forecasts.

- Academic Journals and Publications: Academic papers can offer in-depth analysis and findings on specific market aspects or trends.

- Government and Official Statistics: Government websites often publish industry data, economic statistics, and demographic information that can be invaluable for market analysis.

- Leverage Digital Tools and Databases

- Use online databases and tools like Google Scholar, Statista, and the U.S. Census Bureau to access a wide range of data. Business databases like Bloomberg, Hoovers, and Crunchbase are excellent for financial data and company information.

- Evaluate the Source

- Always consider the source of your information. Look for data from reputable and authoritative sources and check the date of publication to ensure relevance. Be wary of biased information, especially from sources that may have a vested interest in presenting data in a certain light.

- Cross-Verify Information

- Validate the data you collect by cross-checking across multiple sources. This is crucial for ensuring the reliability and accuracy of the information you use in your market analysis.

- Consider the Cultural and Geographic Context

- Ensure the data is relevant to the specific geographic region and cultural context of your target market. Market behaviors can vary significantly across different regions and cultures.

- Utilize Analytical Tools

- Use analytical tools and software for data analysis and visualization. Tools like Excel, Tableau, or Google Analytics can help in organizing data, identifying patterns, and presenting findings in an understandable format.

- Follow Ethical Guidelines

- When conducting primary research, ensure you follow ethical guidelines. Respect privacy, obtain consent, and be transparent about how you will use the data.

- Keep an Eye on Trends

- Use tools like Google Trends to monitor the popularity of certain search terms related to your market. Social media platforms can also provide insights into current consumer interests and discussions.

- Network and Use Professional Contacts

- Leverage your professional network to gain insights and data. Industry insiders can provide valuable information that might not be available through public channels.

By following these tips, you can gather reliable and relevant data for your market analysis, providing a solid foundation for your business strategies and decisions.

What common mistakes should I avoid while conducting a market analysis?

Conducting a market analysis is crucial for understanding your business landscape, but it’s easy to fall into certain traps if you’re not careful. Here are common mistakes to avoid to ensure your market analysis is accurate, relevant, and valuable:

- Overlooking Primary Research

- Relying solely on secondary research can lead to gaps in your analysis. Secondary data might not fully cover your specific market niche or answer all your questions. Incorporate primary research to gather firsthand information about your customers, competitors, and the market.

- Ignoring Industry Trends

- Not staying updated with current trends can make your analysis outdated quickly. Markets evolve, and new trends can significantly impact consumer behavior and competitive landscapes. Always incorporate the latest industry trends and forecasts into your analysis.

- Underestimating the Competition

- Focusing only on direct competitors while ignoring indirect and potential competitors can give you a false sense of security. Indirect competitors offer alternative solutions to the same customer needs and can quickly become direct threats.

- Neglecting Market Segmentation

- Treating the market as a homogenous group without segmentation can lead to inaccurate targeting and positioning strategies. It’s essential to identify different market segments and tailor your strategies to meet the specific needs of each segment.

- Assuming the Market is Static

- A common mistake is to assume that the market conditions when you conduct your analysis will remain unchanged. Markets are dynamic, and various factors, including technological advancements, economic shifts, and regulatory changes, can transform the market landscape. It’s important to anticipate changes and plan accordingly.

- Overreliance on Quantitative Data

- While quantitative data is crucial for understanding market size, growth rates, and other metrics, neglecting qualitative insights can leave you with an incomplete picture. Qualitative data from interviews, focus groups, and surveys can provide deeper insights into consumer behaviors, preferences, and motivations.

- Not Defining the Scope of the Analysis

- Without a clear scope, your market analysis can become too broad or too narrow. Clearly define the geographic, demographic, and product scope of your analysis to ensure it’s relevant to your business objectives.

- Failing to Continuously Update Your Analysis

- Market conditions change, and a one-time analysis won’t stay relevant forever. Regularly updating your market analysis is crucial for staying informed about the latest market developments and adjusting your strategies accordingly.

- Lack of Objectivity

- Confirmation bias, where you only seek out information that confirms your preconceived notions, can skew your analysis. Approach your market analysis with an open mind, ready to discover both positive and negative aspects of the market.

- Poor Presentation of Findings

- Failing to clearly present your findings can make it difficult for stakeholders to understand and act on your analysis. Use clear, concise language and visuals to communicate your findings effectively.

- Ignoring Regulatory and Legal Factors

- Not considering the impact of regulatory and legal factors on your market can lead to unforeseen challenges. Always research and understand the regulatory environment related to your market and industry.

By avoiding these common mistakes, you can ensure that your market analysis is robust, accurate, and actionable, providing a solid foundation for your business strategies.

How frequently should I update my market analysis?

The frequency at which you should update your market analysis can vary depending on several factors, including the volatility of your industry, the growth stage of your business, and significant changes in the market. However, as a general guideline:

- Annually for Routine Updates

- Conduct a comprehensive update of your market analysis at least once a year. This annual review allows you to capture major shifts in the market, such as new competitors, changing customer preferences, technological advancements, and regulatory changes.

- Following Significant Industry Events

- If your industry is subject to rapid changes or if there’s a significant event, like the introduction of disruptive technology, regulatory changes, or economic shifts, you should update your market analysis to reflect these changes. These events can drastically alter the market landscape and require a prompt response.

- When Launching New Products or Services

- Before introducing a new product or service, update your market analysis to ensure that your decisions are based on the latest market data. This helps in understanding the current competitive landscape, consumer needs, and any new trends that could affect the launch.

- During Strategic Planning Sessions

- If your business is undergoing strategic planning or redirection, it’s crucial to have an up-to-date market analysis. This will inform your strategic decisions and help in setting realistic goals and objectives.

- After Significant Business Milestones

- Achieving or failing to achieve a significant milestone (e.g., sales targets, and customer acquisition goals) is a good time to revisit your market analysis. This can provide insights into whether market conditions have changed or if your strategies need adjustment.

- When Entering New Markets

- If you’re considering expanding into new geographic regions or customer segments, conduct a new market analysis focused on these areas. Markets can vary greatly by region and demographics, and assumptions from one market may not hold in another.

Key Considerations for Updating Your Market Analysis:

- Monitoring Tools: Utilize tools and services that monitor the market and industry news. This can help you stay informed about when changes in the market might necessitate an update to your analysis.

- Customer Feedback: Regular feedback from your customers can provide early signals of changing market needs and preferences.

- Competitor Movements: Keep an eye on your competitors. Significant changes in their strategies or offerings may indicate shifts in the market that require your attention.

- Regulatory Environment: Stay updated on any regulatory changes that could impact your industry. These can affect market dynamics significantly.

Conclusion

The exact frequency of updates will depend on your specific circumstances, but staying proactive and keeping your market analysis current is crucial for maintaining a competitive edge. By regularly updating your analysis, you can make informed decisions, identify new opportunities, and respond effectively to market changes.

How can I use the market analysis to identify new growth opportunities for my firm?

Using market analysis to identify new growth opportunities is essential for strategic planning and the long-term success of your firm. A comprehensive market analysis provides insights into industry trends, customer needs, competitive landscapes, and potential areas for expansion or innovation. Here’s how you can leverage your market analysis to uncover new growth opportunities:

- Spot Emerging Trends

- Analyze trends within your industry, including technological advancements, consumer behavior changes, and regulatory shifts. Identifying and acting on emerging trends before they become mainstream can position your firm as a market leader.

- Understand Customer Needs and Gaps

- Use your market analysis to delve deep into customer needs, preferences, and pain points. Look for unmet or underserved needs within your target market segments. Developing solutions that address these gaps can open up new avenues for growth.

- Analyze Competitor Strategies

- Examine your competitors’ strengths and weaknesses, along with their market positioning. Identify areas where your firm can differentiate itself or improve upon competitors’ offerings. Also, pay attention to sectors or niches that competitors are overlooking, which might represent untapped opportunities.