- Understanding the Purpose of Streamlining Accounting Operations

- Overview of Key Areas of Focus for Streamlining Operations

- Assessing Current Operations

- Implementing Technology Solutions

- Streamlining Workflow Processes

- Optimizing Resource Allocation

- Monitoring and Continuous Improvement

- Conclusion

- Download the Workbook

As your accountancy firm scales, streamlining operations becomes critical – not just for day-to-day efficiency but also for strategic growth. Efficient operations free up valuable time and resources, ensuring that your team can focus on core tasks like client advisory, financial analysis, and business development.

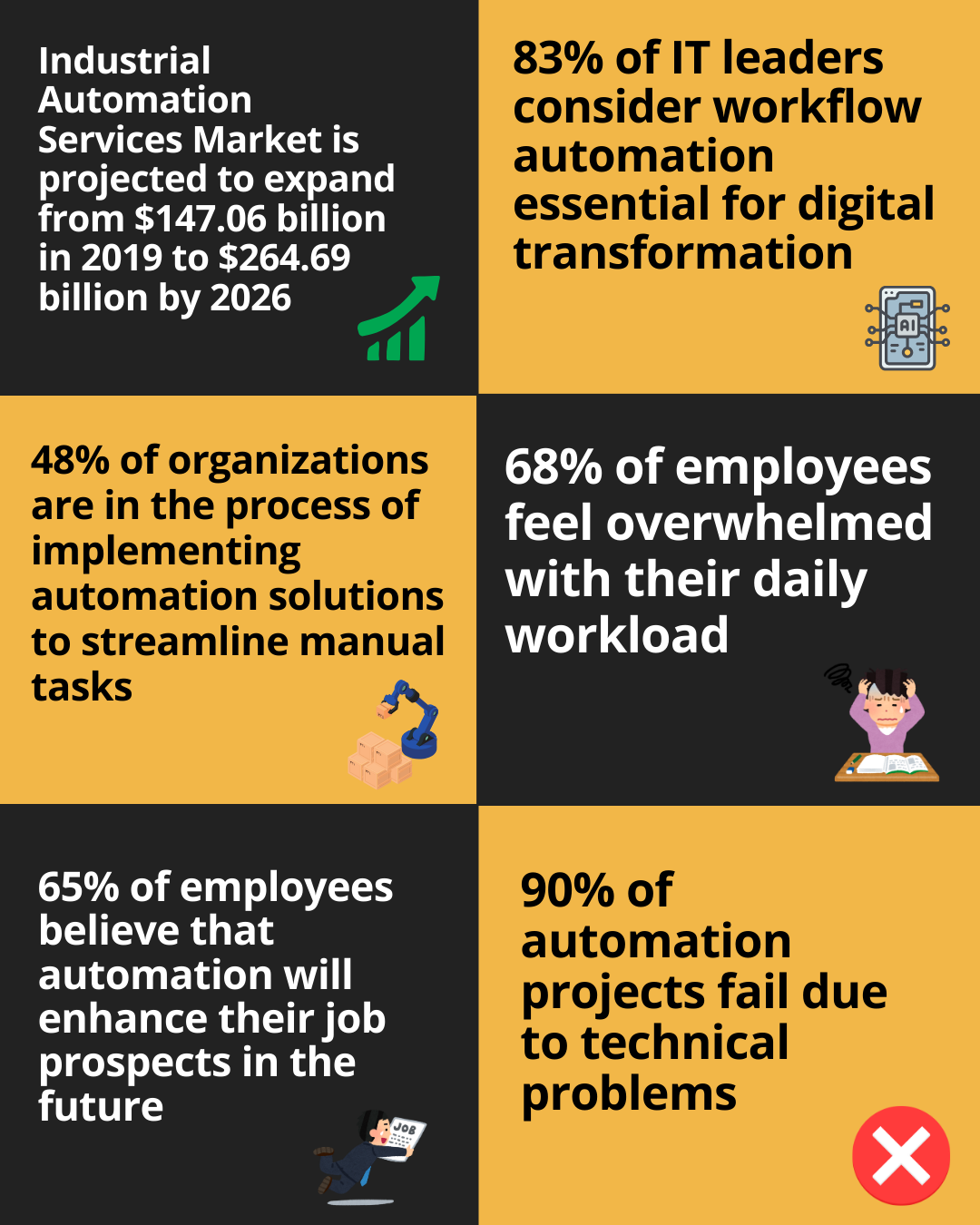

The Industrial Automation Services Market is projected to expand from $147.06 billion in 2019 to $264.69 billion by 2026 [1].

With competition intensifying and clients demanding faster, more accurate services, an optimized operational structure sets your firm apart.

This module is designed to show how streamlining accounting processes isn’t just about cost-cutting or efficiency gains – it’s about transforming your firm into a high-performing, adaptable, and growth-oriented business.

Key Takeaways

- Review your current processes to find inefficiencies.

- Use automation tools to reduce manual work.

- Standardise workflows for consistency and fewer errors.

- Allocate resources smartly based on workload.

- Track and improve regularly to stay efficient.

Understanding the Purpose of Streamlining Accounting Operations

According to Camuda’s The State of Process Automation report, 83% of IT leaders consider workflow automation essential for digital transformation, and 48% of organizations are in the process of implementing automation solutions to streamline manual tasks [2].

Whether you’re managing a small team or overseeing multiple departments, inefficient systems can lead to miscommunication, duplication of work, and missed deadlines, all of which negatively affect client satisfaction. In contrast, a streamlined firm operates like a well-oiled machine, with synchronized processes that deliver faster turnaround times, fewer errors, and improved client experiences.

Maximizing Efficiency

Accounting firms deal with a high volume of repetitive tasks, from transaction recording to compliance checks. Streamlining these processes – through standardization, automation, and smart workflows – ensures that your team spends less time on manual, low-value tasks and more on strategic work. This not only boosts productivity but also enhances job satisfaction, as accountants can focus on high-impact client activities.

Error Reduction

The more manual processes your firm relies on, the higher the risk of mistakes – whether it’s data entry errors, missed deadlines, or compliance oversights. By automating repetitive tasks and standardizing procedures, your firm can significantly reduce these errors, ensuring more accurate financial reporting and stronger client trust. Automation tools and standardized workflows act as a safeguard, minimizing human error and increasing output accuracy.

Cost Savings

Inefficiencies often translate to wasted resources – whether it’s time, staff hours, or financial overheads. By streamlining operations, firms can cut unnecessary expenses and allocate resources more effectively. For example, automating payroll or financial reporting reduces the need for multiple manual reviews, freeing up staff to take on additional clients or projects without requiring extra hires, thus improving your firm’s bottom line.

Improved Client Service

Clients expect speed and precision in today’s fast-moving financial landscape. Streamlined processes allow your team to respond more quickly to client requests, provide timely insights, and deliver consistent results. This builds a strong reputation for reliability and professionalism, helping to retain existing clients and attract new ones. A firm that consistently meets deadlines with precise data is one that clients trust and recommend.

Scalability

As your firm grows, so does the complexity of its operations. Without streamlined processes, growth can lead to operational bottlenecks, which hinder efficiency. Streamlined operations lay the groundwork for scalable systems – enabling your firm to handle increased workload without compromising service quality. Whether you’re managing a growing client base or expanding service offerings, optimized processes allow you to scale efficiently.

Overview of Key Areas of Focus for Streamlining Operations

This module will delve into five essential areas that accountancy firms must address to streamline their operations. Each area is critical to reducing inefficiencies and unlocking the full potential of your firm’s resources:

Automation of Routine Tasks

Routine tasks such as bookkeeping, invoicing, payroll processing, and bank reconciliations can consume a significant portion of your team’s time. Automating these tasks through software like Xero, QuickBooks, or specialized payroll platforms can free up countless hours, allowing staff to focus on value-added services. Automation also improves consistency and reduces the margin of human error, offering more accurate and timely financial data.

Cloud Integration

Moving accounting operations to the cloud centralizes your firm’s data and facilitates real-time collaboration. Cloud-based solutions enable your team to work from anywhere, securely access client information, and provide clients with up-to-the-minute insights into their financial status. The ease of integration across platforms also improves data flow, reducing administrative workload and enhancing operational agility. Additionally, cloud solutions can scale as your firm grows, supporting your operational needs without requiring significant hardware investments.

Workflow Optimization

Streamlining isn’t just about cutting down time – it’s about rethinking the way work flows through your firm. By mapping out existing workflows, identifying bottlenecks, and applying lean principles, you can optimize processes from client onboarding to report generation. Improved workflows ensure that tasks are handled efficiently and that each team member knows their role, eliminating confusion and duplication of effort. This also ensures that client deliverables are completed on time and to the highest standard.

Data Management

The heart of any accounting firm is data – whether it’s financial records, compliance reports, or client information. Efficient data management is key to minimizing errors, improving accessibility, and ensuring data security. Implementing a robust data management system helps in organizing, storing, and retrieving financial information effortlessly. This reduces the time spent searching for files, minimizes security risks, and ensures compliance with regulatory requirements.

Team Training & Development

Even with the best tools and systems in place, your firm will not reach its full potential without a well-trained and motivated team. Investing in ongoing training ensures that your staff stays up-to-date with the latest technology, compliance regulations, and best practices. A skilled team is more productive, capable of delivering higher-quality services, and able to adapt to changing operational demands. Continuous development programs also enhance staff engagement and retention, creating a more stable workforce.

By mastering the strategies outlined in this module, you’ll equip your firm to operate at peak efficiency, delivering better client outcomes while positioning your business for future growth.

Assessing Current Operations

Before you can effectively streamline your accounting firm’s operations, it’s essential to start with a clear understanding of how things work now. Assessing your current operations allows you to identify inefficiencies, bottlenecks, and areas where improvement is needed. By doing this, you lay the groundwork for a more efficient, scalable, and client-focused business.

Due to the fact that 68% of employees feel overwhelmed with their daily workload, companies are increasingly turning to business process automation to help manage tasks more effectively [3].

In this chapter, we will guide you through three critical steps: evaluating your existing processes, gathering feedback, and analyzing performance metrics.

Evaluate Existing Processes

The first step in assessing your current operations is to evaluate your firm’s core processes. Knowing which tasks are essential and how they are currently handled is key to improving them. Here’s how to start:

Identify Key Operations

Begin by listing all the major processes your firm handles daily. Common processes in an accounting firm include:

- Client Onboarding: Bringing new clients into your system and ensuring all necessary documents and agreements are in place.

- Invoicing: Generating and sending invoices to clients for services provided.

- Financial Reporting: Preparing and delivering financial reports for clients, including balance sheets, income statements, and cash flow analysis.

- Compliance Management: Ensuring that all financial activities comply with relevant laws and regulations, such as tax filings and audit requirements.

- Payroll Processing: Managing payroll for clients, ensuring timely and accurate wage calculations, deductions, and tax payments.

By clearly identifying these key operations, you can begin to understand which areas are most crucial to your firm’s efficiency and success.

Review Current Workflow

After identifying your major processes, the next step is to document how each is currently executed. This means breaking down each process into its component tasks and analyzing how they flow from start to finish. For example, how is client onboarding handled? What steps are involved in creating and sending invoices? Document each step and identify any potential bottlenecks or inefficiencies. For instance:

- Are there delays in collecting client information during onboarding?

- Do financial reports require multiple revisions due to errors or miscommunication?

By reviewing these workflows in detail, you’ll be able to spot inefficiencies, duplication of effort, or gaps in communication that may be slowing down your firm.

Gather Feedback

Did you know that half of business leaders intend to increase the automation of repetitive tasks within their organizations [4]? Therefore, to get a well-rounded view of your current operations, it’s important to gather feedback from both your employees and your clients. Their insights can provide a different perspective on where improvements are needed.

Employee Input

Your team is at the heart of your firm’s operations, so their feedback is crucial. In fact, nearly 2/3 (65%) of employees believe that automation will enhance their job prospects in the future [5].

Gather input from your staff about the challenges they face in their daily tasks. This can be done through surveys, interviews, or team meetings. Ask questions such as:

- What tasks are the most time-consuming?

- Where do they encounter bottlenecks or frustrations?

- Are there any tools or resources they believe could make their job easier?

Employees often have firsthand experience with the inefficiencies of current systems and may have valuable suggestions for improving processes. For example, staff members may notice that manual data entry during invoicing slows down the workflow, and automating this process could save time and reduce errors.

Client Feedback

Clients are another critical source of feedback. If they’ve experienced delays, inaccuracies, or frustrations in your service, their complaints or suggestions are valuable data points for identifying operational weaknesses. Consider asking clients for their feedback via surveys or direct communication. Ask questions like:

- How satisfied are you with the timeliness of our services?

- Have you encountered any errors or delays in our reporting or invoicing?

- What improvements could we make to better meet your needs?

Client feedback will not only help you improve your operations but also enhance client satisfaction, which is crucial for retention and growth.

Analyze Performance Metrics

Data-driven decisions are key to successfully streamlining your operations. By analyzing performance metrics, you can objectively measure how well your processes are working and where improvements are needed.

Key Metrics

There are several metrics you can track to gauge the efficiency of your operations. Four key metrics for accounting firms include:

- Processing Time: How long it takes to complete key tasks, such as generating financial reports or onboarding a new client. Long processing times often indicate inefficiencies.

- Error Rates: The frequency of errors in financial reports, invoicing, or payroll. High error rates suggest the need for better training, automation, or process redesign.

- Client Satisfaction: Measured through client feedback, this metric shows how satisfied your clients are with your services. Low client satisfaction often points to issues with timeliness, accuracy, or communication.

- Cost per Process: How much it costs your firm to complete specific processes, such as payroll processing or financial reporting. High costs may indicate that processes are overly manual or inefficient.

Benchmarking

Once you’ve gathered data on these metrics, compare them to industry standards or competitors to assess how well your firm is performing. There are several ways to benchmark your performance:

- Industry Averages: Use industry reports and studies to understand how your firm’s performance stacks up against the average in the accounting industry. For example, how does your average invoicing time compare to industry norms?

- Competitor Analysis: If possible, obtain data from competitors or firms of similar size to see how they manage key processes. This can provide a more direct comparison and reveal where you may be lagging.

- Internal Benchmarks: Track your firm’s performance over time to spot trends. For instance, if your error rates have increased over the past year, it may indicate that a process is becoming outdated or overwhelming.

By analyzing these metrics and benchmarks, you can identify specific areas where your firm needs improvement and set measurable goals for enhancing your operations.

Implementing Technology Solutions

In the modern accounting landscape, technology is the backbone of efficiency and accuracy. By implementing the right technology solutions, your firm can automate repetitive tasks, streamline workflows, and provide clients with faster, more reliable services.

This chapter focuses on how to effectively integrate accounting software, automation tools, and cloud solutions to optimize your firm’s operations. Embracing these technologies not only saves time and reduces errors but also makes your firm more agile and responsive to client needs.

Adopting the Right Accounting Software

Choosing and integrating the right accounting software is crucial for streamlining your operations. The right tools will allow your firm to manage finances, track expenses, and generate reports more efficiently.

Choose the Right Tools

When selecting accounting software, it’s essential to evaluate your firm’s specific needs and workflows. Popular accounting platforms like QuickBooks, Xero, and Sage offer comprehensive solutions for managing client accounts, invoicing, and financial reporting. Each tool has its strengths:

- QuickBooks is well-suited for small to mid-sized firms with robust payroll and expense management features.

- Xero excels in cloud integration and seamless collaboration with clients.

- Sage is ideal for larger firms handling more complex financial operations.

Choosing the right tool depends on your firm’s size, service offerings, and whether you need advanced features like payroll processing, project management, or multi-currency handling. The goal is to select a platform that aligns with your firm’s operational goals and can scale with your growth.

Integration

Once you’ve chosen your software, ensure it integrates seamlessly with other systems used by your firm. For example, your accounting software should sync with your CRM (customer relationship management) system to streamline client onboarding and service delivery.

90% of automation projects fail due to technical problems, and the third most significant obstacle to implementing automation is resistance to change [6]. Integration with payroll systems, time tracking tools, and document management software helps create a unified workflow. This reduces manual data entry, cuts down on errors, and ensures that data flows smoothly across your firm’s operations.

By ensuring smooth integration, your firm can avoid silos of information and operate with a consistent, accurate data stream that benefits both your team and your clients.

Identifying Routine Tasks to Automate

In a 2020 survey, McKinsey found that 66% of businesses had automated processes across multiple functions, up from just 57% in 2018 [7].

One of the biggest benefits of technology in accounting is its ability to automate repetitive tasks. Automating routine processes like invoicing and expense tracking not only saves time but also increases accuracy.

Invoice Automation

Invoicing is a time-consuming task that can easily be automated with the right tools. By setting up automated invoicing, you can reduce the need for manual entry, eliminate the possibility of errors, and ensure that invoices are sent out on time. Software like QuickBooks or Xero can automate recurring invoices, apply late fees automatically, and track payments. This not only speeds up your billing cycle but also improves cash flow as clients are more likely to pay promptly with automated reminders.

Expense Tracking

Manual expense tracking is prone to errors and takes up valuable time. Using expense tracking tools, you can automatically categorize expenses, track receipts, and generate real-time expense reports. Software like Expensify or Receipt Bank allows your team to capture and categorize expenses on the go, ensuring nothing falls through the cracks. Automation of this process saves your accountants from sifting through stacks of receipts or manually categorizing every transaction.

By automating these routine tasks, your firm can focus on more strategic work such as advisory services and financial planning, while also reducing the likelihood of human error in data entry.

Utilizing Time-Efficient Cloud Solutions

Cloud technology has transformed the accounting industry by providing remote access, real-time collaboration, and enhanced data security. According to one survey, nearly one-third of businesses have managed to automate one function at least in full, resulting in significant time savings [8].

Utilizing cloud-based solutions gives your firm the flexibility to work from anywhere while ensuring data is always up-to-date and accessible.

Access Anywhere

Cloud-based accounting platforms like Xero or Sage allow your team to access client data from anywhere, at any time. This flexibility is crucial in today’s increasingly remote and hybrid work environments. With cloud solutions, your firm can collaborate in real time, ensuring that client reports, financial statements, and other essential documents are updated as soon as new data is entered. Remote access also improves client relationships by enabling faster turnaround times on requests and seamless collaboration.

Data Security

While cloud solutions offer convenience, security must be a top priority. Ensure that your cloud provider offers strong security features such as encryption, multi-factor authentication, and regular data backups. Protecting sensitive client financial data is non-negotiable in the accounting industry. Leading cloud providers like Google Cloud, AWS, and Microsoft Azure offer robust security measures that safeguard data against breaches. Additionally, ensure that your internal team follows best practices for access control and data protection, reinforcing the security infrastructure provided by your cloud services.

Implementing the right technology solutions is a key step toward building a streamlined, efficient, and scalable accounting firm. By adopting the right accounting software, automating routine tasks, and leveraging cloud solutions, your firm will be able to save time, reduce errors, and deliver better services to clients. In the next chapter, we will explore how to optimize workflows and enhance your firm’s overall operational structure.

Automated Alternatives

| Manual Task | Automated Alternative |

|---|---|

| Data entry from receipts | OCR (Optical Character Recognition) tools like Dext or AutoEntry |

| Chasing unpaid invoices | Automated payment reminders via accounting software (e.g. Xero, QuickBooks) |

| Bank reconciliation | Auto-matching with bank feeds in cloud accounting platforms |

| Client onboarding emails | Pre-set workflows and email automation through CRMs like Karbon |

| Document sharing and signing | E-signature tools like Adobe Sign or HelloSign |

| Monthly reporting | Scheduled reporting dashboards and templates |

Streamlining Workflow Processes

Efficient workflow processes are essential for accounting firms looking to improve operational efficiency, reduce errors, and deliver consistent services to clients. Streamlining workflows ensures that every task, from client onboarding to financial reporting, is executed with precision and efficiency.

In this chapter, we explore how standardizing procedures, enhancing communication, and improving project management can lead to a more organized and productive accounting firm.

Standardize Procedures

With 24% of companies already using low-code process automation systems and another 29% planning to adopt them soon, these platforms drive efficiency by streamlining workflows, optimizing data use, and saving time and money [9].

One of the most effective ways to streamline workflows is by standardizing procedures across your firm. Consistency in how tasks are performed ensures that all team members follow best practices, reducing errors and increasing efficiency.

Document Processes

Creating detailed process documentation is key to achieving consistency. Here are 5 ways to approach this:

- Flowcharts: Visualize each step of a process to ensure clarity and understanding.

- Step-by-Step Guides: Provide detailed written instructions for tasks like invoicing, reporting, or client onboarding.

- Checklists: Create task-specific checklists to ensure nothing is overlooked.

- Video Tutorials: Develop video guides to train employees in complex procedures, making it easier for new staff to follow.

- Centralized Access: Store all documentation in a central repository (like Google Drive or a firm-wide intranet) so everyone has access to up-to-date procedures.

By documenting every process clearly, you reduce confusion and ensure that tasks are carried out consistently, regardless of who is responsible.

Develop Templates

Using templates for common tasks can save time and ensure uniformity across the firm. Here are 3 key benefits of utilizing templates:

- Consistency: Templates ensure that reports, invoices, and client communications follow the same format every time.

- Time Savings: By reducing the need to create documents from scratch, templates allow your team to focus on more complex tasks.

- Error Reduction: Pre-designed templates reduce the chances of missing key information or making formatting mistakes.

Templates for financial reports, client updates, and internal documents make processes faster and ensure that the firm presents a professional and organized image to clients.

Enhance Communication

Effective communication is at the heart of streamlined workflows. Without clear and efficient communication, tasks can fall through the cracks, deadlines can be missed, and both staff and clients can feel frustrated.

Internal Communication

Implementing communication tools like Slack or Microsoft Teams can transform how your team collaborates. Here are 3 reasons why internal communication tools are essential:

- Real-Time Collaboration: These platforms allow teams to communicate in real time, making it easier to resolve issues and share information quickly.

- Centralized Conversations: By creating specific channels for each project or client, team members can easily access relevant conversations and files.

- Remote Accessibility: As many firms embrace hybrid or remote work models, communication tools ensure that all team members stay connected, regardless of location.

These tools help streamline internal communication, allowing for faster decision-making and fewer delays in task completion.

Client Communication

Streamlining client communication is just as important as internal collaboration. Here are 4 ways to improve client interactions:

- Automated Emails: Use automated email reminders for upcoming deadlines, payments, or document submissions to ensure clients stay on track.

- Client Portals: Implement client portals where clients can upload documents, view reports, and track the progress of their projects.

- Email Templates: Standardize client communications with pre-written email templates for common scenarios such as onboarding, invoicing, or report delivery.

- Regular Updates: Set up automatic client updates on the status of their projects to keep them informed without requiring constant manual follow-ups.

These strategies ensure that clients are always informed and engaged while reducing the manual workload for your team.

Improve Project Management

Managing projects efficiently is crucial for meeting deadlines, tracking progress, and ensuring client satisfaction. The right project management tools and clear deadlines help keep your firm organized and accountable.

In fact, consistently applying project management practices leads organizations to a 92% success rate in achieving project objectives [10].

Task Management Tools

Utilizing project management tools like Asana, Trello, or ClickUp can have a significant impact on how tasks are managed within your firm. Here are 4 benefits of using these tools:

- Visibility: Track all tasks and projects in one place, making it easier to see who is responsible for what and when it’s due.

- Accountability: Assign tasks to specific team members, ensuring everyone knows their responsibilities.

- Deadline Tracking: Set deadlines for each task, helping your team stay on schedule and avoid last-minute rushes.

- Collaboration: Team members can collaborate on tasks by sharing updates, files, and comments directly within the platform.

These tools enhance productivity by making it easier to manage workloads and avoid missing important deadlines.

Set Clear Deadlines

Establishing and communicating clear deadlines for all tasks and projects is critical to maintaining an organized workflow. Here are 5 reasons why clear deadlines are important:

- Focus: Deadlines provide a clear endpoint for each task, helping employees prioritize their workload.

- Accountability: Setting deadlines ensures that team members are responsible for completing tasks on time.

- Client Satisfaction: Meeting deadlines improves client trust and satisfaction, as they receive timely reports and services.

- Project Visibility: Clear deadlines make it easier to track progress and identify potential bottlenecks before they become issues.

- Consistency: When deadlines are met effectively, the firm operates more smoothly, reducing the risk of delays.

Streamlining workflow processes is about creating a smooth, consistent, and efficient way of managing tasks and communication within your firm. By standardizing procedures, enhancing both internal and client communication, and improving project management, your accounting firm can achieve greater operational efficiency, leading to better performance and improved client satisfaction.

Optimizing Resource Allocation

Optimizing resource allocation is a strategic priority for accounting firms looking to enhance efficiency, control costs, and grow their business. The goal is to ensure that the right resources—staff, technology, and external services—are aligned with the firm’s needs to maximize productivity without overspending.

This chapter explores the critical steps in evaluating staffing, leveraging outsourcing, and managing costs effectively. By optimizing how resources are allocated, firms can achieve better client service and improved profitability.

Evaluate Staffing Needs

Staffing is one of the largest operational expenses in an accounting firm. Ensuring that your team is properly resourced and that employees have the necessary skills to meet client demands is essential. The key is to assess current roles, workloads, and development needs so you can adjust your staffing levels for peak efficiency.

Role Assessment

Assessing your team’s structure and responsibilities is the first step in optimizing resource allocation. On the upside, nearly 3/4 of employees are willing to learn new skills or retrain to stay employable, believing it’s their responsibility to upskill rather than depend on employers [11].

Here’s how you can thoroughly review staffing levels and roles:

- Evaluate Job Role Effectiveness: Look at whether each role is effectively aligned with its intended responsibilities. For example, if your junior accountants are spending too much time on administrative tasks, they might not be contributing enough to core accounting functions. Restructuring or delegating lower-priority tasks could free up their time for more valuable work.

- Assess Capacity Utilization: Are your staff working at full capacity, or are some overworked while others are underutilized? For example, during tax season, the tax compliance team might be overwhelmed while the advisory team has downtime. Redistributing tasks can balance the workload and reduce burnout.

- Identify Role Redundancies: Look for overlap in roles or tasks. For example, if two team members are handling client onboarding and another team member is managing documentation separately, consolidating these roles could improve efficiency and communication.

- Determine Core vs. Non-Core Roles: Distinguish between essential roles that directly drive revenue, such as tax consultants and auditors, and non-core roles like IT support or HR. Focusing your in-house resources on revenue-generating activities while outsourcing non-core functions can increase profitability.

- Analyze Long-Term Staffing Needs: Consider how future growth might affect your staffing needs. For example, if your firm plans to expand into a new market, you may need to start building expertise or hiring specialists in that area.

By periodically assessing and adjusting roles, you can ensure your staff is aligned with business priorities, maximizing productivity and avoiding overstaffing or role misalignment.

Training and Development

Once you’ve assessed your staffing structure, it’s crucial to identify any skills gaps that could be limiting your team’s efficiency and effectiveness. Here’s how you can enhance employee capabilities through targeted training:

- Skill Audits: Perform a comprehensive review of your team’s skills. For instance, with new accounting software or tax regulations constantly evolving, certain team members may lack expertise in specific areas, such as cloud accounting or international tax laws.

- Tailored Training Programs: Based on the audit, provide customized training that directly addresses the firm’s needs. If your firm is embracing automation or new software tools like QuickBooks or Xero, investing in technical training can boost team productivity and accuracy.

- Cross-Training for Flexibility: Train your staff to handle tasks outside their core roles, such as teaching tax accountants how to assist with bookkeeping during peak periods. Cross-training provides your firm with greater flexibility and ensures you can respond to fluctuations in workload without needing to hire additional staff.

- Mentorship and Career Development: Establish mentorship programs where senior accountants provide guidance to juniors, helping them develop specialized skills. This not only enhances professional growth but also boosts employee retention by offering clear career development paths.

Training and development are investments that enhance staff performance, making the firm more responsive to client needs and future growth opportunities.

Outsource Non-Core Functions

Outsourcing non-core activities allows accounting firms to concentrate on delivering core services while delegating specialized or time-consuming tasks to external providers. Done strategically, outsourcing can improve efficiency and reduce costs without sacrificing quality.

In fact, 37% of IT customer service departments achieve a higher return on investment from automation than any other department [12].

Identify Opportunities

Identifying the right functions to outsource requires careful analysis of both cost and complexity. Here are five key areas where outsourcing could benefit your firm:

- IT Support: Managing an in-house IT team can be costly and inefficient, especially for smaller firms. Outsourcing IT management, such as cloud hosting, cybersecurity, and network maintenance, ensures that your systems remain secure and up to date without burdening your internal staff.

- Payroll and Benefits Administration: Payroll is a critical but non-revenue-generating task. Outsourcing payroll management ensures accuracy, compliance with tax regulations, and timely processing without diverting internal resources.

- Legal Compliance: Accounting firms often deal with complex legal issues, such as regulatory compliance or client contract reviews. Outsourcing to specialized legal professionals ensures that these matters are handled correctly, reducing legal risks.

- Marketing and Lead Generation: Instead of employing a full-time marketing team, outsourcing your firm’s marketing efforts to an agency that specializes in accounting services can drive better results for lead generation, SEO, and brand management.

- Bookkeeping Services: For firms focused on high-level advisory services, outsourcing bookkeeping can free up time for more valuable tasks like financial planning and consulting, without reducing service quality for clients.

By identifying non-core functions and strategically outsourcing them, you free up time and resources to focus on higher-margin services that directly contribute to the firm’s growth.

Select Providers

Choosing the right outsourcing provider is critical to ensure that your outsourced tasks are managed efficiently and meet your firm’s quality standards. Here’s how you can make that decision:

- Evaluate Expertise and Reputation: Ensure the outsourcing firm has a proven track record in your industry. For instance, if you’re outsourcing bookkeeping, the provider should specialize in working with accounting firms and have expertise in your particular software.

- Ensure Seamless Integration: Verify that the service provider’s systems integrate smoothly with your firm’s software, such as accounting platforms and CRMs, to avoid workflow disruptions.

- Consider Communication and Support: Look for outsourcing partners that provide strong customer support and clear lines of communication. It’s essential that you can easily reach them for troubleshooting or when urgent matters arise.

- Test Before Committing: Before signing long-term contracts, consider starting with a short-term or pilot project to evaluate their performance. This trial phase allows you to gauge the quality of service and ensure they meet expectations.

Selecting reliable outsourcing partners ensures that non-core tasks are handled efficiently, allowing you to focus on core business services and client satisfaction.

Cost Management

Cost management is an ongoing effort that requires accounting firms to regularly review their operating expenses and seek out opportunities for savings. Keeping costs under control without compromising service quality is key to maintaining profitability.

Review Expenses

A thorough, regular review of operating expenses can reveal unnecessary spending and areas for cost reduction. Here’s how to approach this:

- Audit Vendor Contracts: Evaluate all existing contracts with vendors, such as IT services, office supplies, or software licenses. If you find that your firm is paying for services you don’t fully use or that there are cheaper alternatives, it’s time to renegotiate or switch providers.

- Analyze Technology Spending: Ensure that your firm’s technology investments are being fully utilized. For example, if you’re paying for features within your accounting software that you rarely use, consider scaling back your subscription plan.

- Assess Overhead Costs: Overhead, including rent, utilities, and office supplies, can quickly accumulate. Regularly review these expenses to identify areas where you can save, such as switching to energy-efficient utilities or reducing unnecessary office space.

- Benchmark Against Industry Averages: Compare your firm’s expenses with industry benchmarks to ensure your cost structure is competitive. This allows you to see where your costs are out of line and make informed decisions to bring them back in line with best practices.

Regularly reviewing expenses ensures that your firm is not wasting money on outdated services or unnecessary overhead, keeping your operating costs lean and efficient.

Negotiate Contracts

Contract negotiation is a powerful tool for managing costs. Here’s how to get the best deals from vendors and service providers:

- Research Market Prices: Before renewing contracts, research the market to see what competitors are offering. Use this data as leverage to negotiate better pricing with your current vendors.

- Negotiate Volume Discounts: If your firm anticipates growth, negotiate bulk discounts or long-term pricing with your vendors. Committing to larger service volumes or longer contracts can often result in substantial cost savings.

- Ask for Flexible Terms: Request terms that allow you to scale services up or down depending on your firm’s needs. This flexibility can help your firm avoid overpaying for services during slow periods.

- Bundle Services: Where possible, bundle services with the same provider. For example, if a vendor offers both IT support and cloud services, negotiating a bundled contract can lead to cost reductions.

- Review Contracts Annually: Make it a practice to review all contracts annually to ensure that your firm is still receiving the best possible terms. This also allows you to renegotiate if the value of the contract has diminished over time.

Optimizing resource allocation is essential to driving efficiency and profitability in an accounting firm. By evaluating staffing needs, outsourcing non-core functions, and managing costs effectively, firms can streamline operations, reduce expenses, and focus on delivering higher-value services to clients.

Monitoring and Continuous Improvement

For an accounting firm to stay competitive and deliver top-notch service, monitoring operations and making continuous improvements is crucial. Streamlining workflows and implementing new tools is just the beginning; the real value comes from ongoing review and refinement.

This chapter explores the essential practices of tracking performance, gathering feedback, and making strategic adjustments. By embracing a culture of continuous improvement, your firm can adapt to changes, improve efficiency, and maintain high levels of client satisfaction.

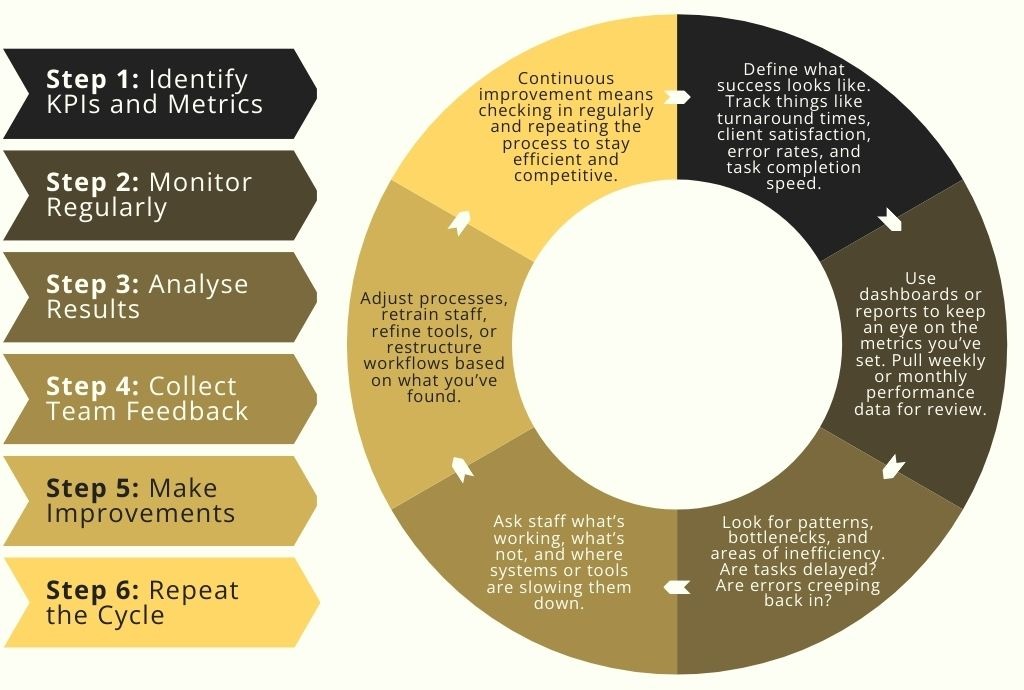

Track Performance

Tracking performance is about more than just checking off tasks; it’s about ensuring that every process, every tool, and every employee contributes to the firm’s goals of efficiency, accuracy, and client satisfaction. To achieve this, firms must establish regular performance reviews and monitor key metrics to measure the effectiveness of the changes they’ve implemented.

Regular Reviews

Setting up regular performance reviews ensures that your firm continuously assesses the impact of any changes made to streamline operations. Here are four key reasons why regular reviews are important:

- Identify Ongoing Issues: Without frequent check-ins, inefficiencies or bottlenecks that may have arisen from new processes can go unnoticed. For instance, newly implemented software may initially improve workflow but create unexpected delays as employees adjust to it.

- Measure Improvement: Performance reviews provide a structured opportunity to measure whether operational improvements are having the desired effect, such as reducing processing times or improving accuracy in financial reports.

- Ensure Accountability: Regular reviews hold teams accountable for their role in the firm’s processes. By reviewing performance metrics regularly, management can ensure employees are aligned with the firm’s overall goals.

- Facilitate Proactive Management: Ongoing reviews allow firms to be proactive rather than reactive. Rather than waiting for a significant problem to emerge, regular check-ins enable management to catch minor issues early and adjust before they escalate.

Frequent reviews should include both operational assessments and feedback from staff, offering a comprehensive view of the firm’s performance.

KPI Tracking

Key performance indicators (KPIs) help firms measure how well they are achieving specific operational goals. In an accounting firm, KPIs can be essential to monitoring efficiency, client satisfaction, and profitability. Here are five ways to effectively track KPIs:

- Client Retention Rates: Retention is a direct indicator of client satisfaction. A firm with a high retention rate is likely offering valuable, consistent service. If retention drops, it signals the need for a closer look at client relationships and service quality.

- Turnaround Times: Monitor the time it takes for tasks such as completing financial reports or filing tax returns. A decrease in turnaround time typically signals improved operational efficiency.

- Error Rates: Tracking how often mistakes occur in financial reporting, client onboarding, or tax filings helps firms identify areas where more training or better tools may be required.

- Billable Hours Utilization: Measure how effectively your team is spending its time. High billable hours utilization indicates that staff are focused on revenue-generating tasks rather than administrative duties.

- Client Acquisition Costs: By tracking the costs involved in acquiring new clients, firms can determine if their marketing and sales efforts are cost-effective. A rising acquisition cost might signal inefficiencies in your lead generation processes.

Tracking these KPIs allows accounting firms to measure the effectiveness of their operational improvements and make data-driven decisions about further adjustments.

Solicit Feedback

Feedback is essential for continuous improvement. It provides valuable insight into what’s working and where adjustments are needed. Both internal staff and external clients can offer different perspectives on operational efficiency and service quality.

Internal Feedback

Encouraging feedback from employees ensures that management remains aware of any challenges or inefficiencies in the firm’s internal processes. Here are four reasons why ongoing internal feedback is crucial:

Encourage an open-door policy or regular feedback sessions where employees can share their insights and suggestions for process improvements.

- Uncover Hidden Issues: Employees are often aware of inefficiencies or pain points that management may overlook. For example, staff might experience delays in accessing critical software tools or find certain workflows overly complex.

- Empower Employees: Soliciting feedback gives employees a sense of ownership in the process. When they feel heard, they are more likely to engage with and support operational changes.

- Improve Morale and Engagement: Employees who have a say in how processes are managed are generally more satisfied with their work environment. In turn, this can lead to increased productivity and lower turnover.

- Refine Operational Adjustments: Feedback from staff can help identify areas where newly implemented changes may not be delivering the intended benefits, allowing management to fine-tune these strategies.

Client Feedback

Clients are the best source of information regarding how well your firm is meeting service expectations. Regularly gathering feedback from clients is essential for improving service delivery. Here are five ways to effectively collect and use client feedback:

- Client Surveys: Sending periodic surveys allows clients to provide detailed feedback on their experience with your firm. This can help identify areas of dissatisfaction, such as communication delays or billing confusion.

- Client Satisfaction Scores: Use tools such as Net Promoter Score (NPS) to track client satisfaction over time. A high NPS indicates that clients are happy with your services and would recommend your firm to others.

- Review Client Complaints: Regularly review any complaints to identify recurring issues. For instance, if multiple clients mention difficulties in accessing online portals, this signals a need for technical improvements.

- Client Interviews: In-depth conversations with key clients can provide a deeper understanding of their expectations and experience with your firm’s services.

- Monitor Online Reviews: Keep an eye on reviews left on public platforms such as Google or LinkedIn. These reviews can offer insight into how the general market perceives your firm.

Collecting client feedback ensures that your firm continuously adapts to client needs, improving client retention and satisfaction over time.

Adjust Strategies

Continuous improvement requires a commitment to adapting strategies based on feedback and performance data. The ability to pivot when something isn’t working as expected is key to sustaining long-term success.

Iterate and Improve

The ability to iterate and improve is central to the idea of continuous optimization. Here are five ways to consistently adjust processes and strategies to ensure operational efficiency:

- Review Feedback Regularly: Continuously monitor both staff and client feedback. Rather than waiting for issues to become urgent, adjust as soon as potential problems are identified.

- Test and Refine Changes: Before fully committing to new strategies or processes, test them on a smaller scale. For example, if implementing a new invoicing system, trial it with a subset of clients to ensure it works as expected.

- Be Open to Revisions: Accept that not every improvement will work as intended. If a new system or process doesn’t deliver the expected results, be prepared to go back and revise it.

- Leverage Data Analytics: Use data from your KPI tracking to refine processes based on real-time performance. If a certain metric, such as turnaround time, shows a downward trend, analyze the underlying causes and address them.

- Encourage a Continuous Improvement Culture: Foster a workplace environment where ongoing improvement is embraced. Staff should feel comfortable experimenting with new ideas and suggesting process changes, knowing that innovation is encouraged.

Iterating based on feedback and data keeps your firm agile and responsive, ensuring it can quickly adapt to challenges or inefficiencies.

Stay Updated

The accounting industry is continuously evolving, with new technologies and practices emerging regularly. Staying updated on these developments helps firms maintain a competitive edge. Here are four ways to stay informed:

- Follow Industry News: Keep up with industry publications and blogs that cover accounting trends, regulatory changes, and best practices.

- Attend Conferences and Webinars: Regularly participate in industry events where new tools, software, and strategies are discussed. These forums are excellent opportunities to stay ahead of the curve.

- Maintain Certifications: Encourage staff to continuously update their professional certifications and participate in continuing education. This ensures your team is always equipped with the latest knowledge and skills.

- Engage in Peer Networking: Networking with other accounting professionals offers valuable insights into emerging trends and innovative practices that your firm might benefit from.

Continuous improvement is a critical component of maintaining a successful, efficient accounting firm. By tracking performance, soliciting feedback, and remaining adaptable, your firm can continuously refine its operations and provide higher levels of service.

Conclusion

Streamlining operations is not just about improving efficiency—it’s about creating a foundation for long-term growth and sustainability in your accounting firm. Throughout this course, we’ve explored actionable strategies that accounting firms can implement to optimize their operations, enhance client satisfaction, and position themselves as leaders in the industry.

As we conclude, it’s important to revisit the key takeaways and encourage a mindset of continuous improvement.

Recapping Key Points

In this course, we discussed the importance of streamlining accounting operations and outlined several key strategies for improving workflow, integrating technology, and optimizing resource allocation. Here’s a recap of the essential strategies:

- Assess Current Operations: By evaluating existing processes, firms can identify bottlenecks and inefficiencies that hinder performance. Tracking key performance metrics is essential for measuring the impact of process improvements.

- Implement Technology Solutions: Utilizing the right accounting software, automating routine tasks, and adopting cloud solutions help firms operate more efficiently, reduce manual errors, and enhance collaboration.

- Streamline Workflow Processes: Standardizing procedures and using templates ensure consistency in service delivery, while enhancing communication and project management improves both internal workflows and client interactions.

- Optimize Resource Allocation: Ensuring the right staffing levels, offering ongoing training, and outsourcing non-core tasks allow firms to focus on high-value activities, improving both efficiency and profitability.

- Monitor and Continuously Improve: Tracking performance, soliciting feedback, and remaining adaptable are key to long-term success. Firms must remain proactive in making adjustments based on data and evolving industry trends.

These strategies not only make operations more efficient but also position your accounting firm to deliver better service, reduce costs, and stay competitive in an ever-changing market.

Time to Action

Now that you have a clear understanding of how streamlining can benefit your firm, it’s time to take action. Start by reviewing your current processes and identifying areas where you can apply these strategies. Here’s why implementing these changes is essential:

- Efficiency Gains: Streamlining your firm’s operations will save time, allowing your team to focus on more value-added tasks such as advisory services, instead of getting bogged down by administrative duties.

- Improved Client Satisfaction: Consistent communication, timely service, and efficient processes lead to happier clients. Satisfied clients are more likely to stay with your firm and refer new business.

- Cost Savings: By optimizing resource allocation and leveraging automation, you can reduce operating expenses, ultimately increasing your firm’s profitability.

- Future-Proofing: Staying ahead of technological advancements and industry trends ensures that your firm remains relevant and competitive.

Starting small is fine. You don’t need to overhaul every aspect of your firm at once. Focus on one or two key areas—whether it’s automating invoicing, implementing a new project management tool, or improving client communication—and build from there.

Download the Workbook

Streamlining accounting operations is critical for optimizing your firm’s performance and ensuring sustainable growth. By refining processes, adopting the right technology, and continuously improving workflows, your firm can reduce inefficiencies, enhance client service, and improve profitability. Streamlined operations also allow you to better allocate resources and focus on high-value activities like advisory services. To support you in this journey, we invite you to download the “Streamlining Operations for Accountancy Firms Workbook.” This resource offers practical tools, templates, and actionable guidance to help you implement the strategies discussed in this module effectively.

Download the Streamlining Accounting Operations Workbook:

Bibliography

- https://www.globenewswire.com/en/news-release/2022/04/28/2431897/0/en/Industrial-Automation-Services-Market-Projected-to-Grow-from-USD-147-06-Billion-in-2019-to-USD-264-69-Billion-by-2026-Report-by-Market-Research-Future-MRFR.html

- https://camunda.com/wp-content/uploads/2020/10/Camunda-State-Of-Process-Automation.pdf

- https://www.cornerstoneondemand.com/resources/article/cornerstone-study-finds-extreme-workloads-are-destroying-employee-productivity/

- https://www.pwc.com/gx/en/services/people-organisation/workforce-of-the-future/workforce-of-the-future-the-competing-forces-shaping-2030-pwc.pdf

- https://www.pwc.com/gx/en/services/people-organisation/workforce-of-the-future/workforce-of-the-future-the-competing-forces-shaping-2030-pwc.pdf

- https://www2.deloitte.com/us/en/insights/focus/technology-and-the-future-of-work/intelligent-automation-2020-survey-results.html

- https://www.mckinsey.com/capabilities/operations/our-insights/the-imperatives-for-automation-success

- https://profiletree.com/business-automation-statistics/

- https://www2.deloitte.com/us/en/insights/focus/technology-and-the-future-of-work/intelligent-automation-2020-survey-results.html

- https://www.visual-planning.com/en/blog/project-management-statistics

- https://www.pwc.com/gx/en/services/people-organisation/workforce-of-the-future/workforce-of-the-future-the-competing-forces-shaping-2030-pwc.pdf

- https://www.salesforce.com/content/dam/web/en_us/www/documents/platform/it-leaders-fueling-time-and-cost-savings-with-process-automation.pdf

About the Author

Rajat Kumar

Rajat is a finance and marketing professional with years of proven experience working in finance and investment KPOs.

Working with Samera’s business development experts, he specialises in creating tips, reports and articles helping accountants understand the global landscape, strategise and grow their business.

Reviewed by

Arun Mehra

Samera CEO

Arun, CEO of Samera, specialises in building global accounting businesses.

Arun is a recognized authority on offshoring and Global Capability Centers (GCCs), having built a global team with locations in the UK and India. He helps other accounting firms leverage offshoring to access global talent, improve efficiency, and future-proof their operations.